- The founder of Vanguard, Jack Bogle, says that over the next decade a conservative portfolio of bonds will only return about 3% a year and stocks about 4% a year.

- However, returns can be improved with a dynamic asset-allocation strategy that adjusts stock- and bond-fund holdings in a retirement account according to market climate.

- The Vanguard LifeStrategy Moderate Growth Fund (VSMGX) holds static investments of 60% equity and 40% bond funds and is compared to our dynamic strategy model.

- Our iM-DMAC(60:40) model, designed for retirement saving and withdrawal management, holds identical assets as VSMGX in up-market conditions but switches to 100% bond funds during equity down-market periods.

- The result, the iM-DMAC(60:40) vastly outperforms VSMGX.

Blog Archives

Improve on Vanguard LifeStrategy Growth Funds with a Dynamic Strategy

How to Avoid the Coming Bear Market Indicated by Shiller’s CAPE Ratio

- The Cyclically Adjusted Price to Earnings Ratio (CAPE ratio) is at 30.2, a very high level which signals overvaluation of stocks and low forward returns, according to Shiller.

- This level was only exceeded twice in the last 136 years, from Aug-1929 to Sep-1929 and from Jun-1997 to Jan-2002, with market declines of 77% and 45% then recorded.

- The Moving Average CAPE Ratio Methodology used here references stock market valuation to a 35-year moving average of the Shiller CAPE ratio instead of the 1881-2017 long-term average.

- Based on the 35-year moving average methodology, historic market performance points towards continuing up-market conditions, possibly for a number of years.

- To avoid the bear market, exit stocks when the spread between the 5-month and 25-month moving averages of S&P-real becomes negative and simultaneously the CAPE-Cycle-ID score is 0 or -2.

Shiller warns in his recent commentary The Coming Bear Market? :

Read more >

Profiting from Market Volatility with the “Anti-VIX” ETN ZIV

- The “Anti-VIX” ETN ZIV is designed to increase in value when the volatility of the S&P 500 decreases, as measured by the prices of VIX futures contracts.

- The model buys ZIV only during up-markets when the VIX > 17 and rising, otherwise during up-markets it buys either QLD or DDM, or IEF when upmarket conditions are absent.

- A backtest of the model from Jan-2011 to Jul-2017 produced a high 60% annualized return with a maximum drawdown of -16% with only 41realized trades.

Profiting from Market Volatility with the “Anti-VIX” ETF SVXY

- The “Anti-VIX” ETF SVXY is designed to increase in value when the volatility of the S&P 500 decreases, as measured by the prices of VIX futures contracts.

- Extended data of SVXY, the ProShares Short VIX Short-Term Futures ETF, from Jan-2006 to the fund’s inception date was calculated from its proxy, the S&P 500 VIX Short-Term Futures Index.

- SVXY is intended for short-term use. Using the extended price data, a buy-and-hold strategy of the hypothetical SVXY resulted in a huge loss of over 90% from 2007 to 2009.

- The model buys SVXY only during up-markets when the VIX > 17 and rising, otherwise during up-markets it buys either QLD or DDM, or IEF when upmarket conditions are absent.

- A backtest of the model from Jan-2007 to Jul-2017 produced a high 70% annualized return with a maximum drawdown of -27% with only 76 realized trades.

Beating Vanguard’s Large-Cap ETFs with a Tax Efficient Capital Strength Portfolio of the Russell 1000

- This system invests in well capitalized companies with strong market positions, which pay good dividends, have price appreciation potential, and provide a degree of downside protection during bear markets.

- The portfolio is quarterly rebalanced and reconstituted, and consists of six large-cap stocks with Capital Strength type characteristics from the Russell 1000 Index, typically held for at least one year.

- A backtest, from Jan-2000 to end of Jun-2017, showed a 17.7% annualized return with a maximum drawdown of -23.3% and a low average annual turnover of about 70%.

- A comparison with Vanguard’s large-cap ETFs older than 10 years shows that for all listed investment periods the Portfolio would have produced higher returns than any of the five ETFs.

Performance Update of the Best10(VDIGX)-Trader: Trading the Stocks of the Vanguard Dividend Growth Fund – VDIGX

- The Vanguard Dividend Growth Fund-VDIGX is closed to new investors. Want-to-be investors can possibly do better than the fund by investing only in a few positions of the fund’s holdings.

- The iM-Best10(VDIGX)-Trader relies on the expertise of the Vanguard’s advisors to make the primary stock selection. VDIGX currently holds 45 large-cap stocks from which the Trader periodically picks its stocks.

- The Trader invests in the ten highest ranked stocks of VDIGX. This strategy, postulated in 2014, has produced to Jun-2017 a 3-year return of more than double that of VDIGX.

- The 3-year performance of the Trader was 64.1% versus 28.4% for VDIGX, giving an excess return of 35.7%. Trading frequency was low, with positions held on average for 126 days.

The iM-Standard 5 ETF Trader (Excludes Leveraged ETFs)

- This system always holds five ETFs (equity-, fixed income-, short equity-, and Gold-ETFs) selected according to stock market climate and rank.

- Typically, during good-equity markets it holds equity-ETFs, and during bad-markets fixed income-ETFs and/or short equity-ETFs. Also at times it can hold three gold-ETFs with other ETFs.

- A one factor ranking system selects five ETFs from a preselected list of 29 ETFs. A simulation from 2000 to 2017 shows a 24% annualized return with a maximum drawdown of -12%.

A Buy Signal from the iM-Enhanced Inflation Timer

- Stocks usually perform poorly when inflation is on the rise. We developed a market timer according to two inflation rate based rules. A buy signal has now emerged.

- Switching according to the signals between the S&P500 with dividends and a money-market fund would have provided from Aug-1953 to end of Jan-2017 an annualized return of 12.69%.

- Over the same period buy-and-hold of the S&P500 with dividends showed an annualized return of 10.08%, producing about a quarter of the total return of the Timer model.

- The Enhanced Inflation Timer uses one additional criterion in the buy rule for stocks (and sell rule for bonds); high-beta stocks must perform better than low-beta stocks.

How to Beat the First Trust Capital Strength ETF (FTCS) and Other Large-Cap ETFs with the Capital Strength Stocks of the Russell 1000

- This system invests in well capitalized companies with strong market positions, which pay good dividends, have price appreciation potential, and provide a degree of downside protection during bear markets.

- The portfolio holds six large-cap stocks selected from a universe of twenty Russell 1000 Index stocks with Capital Strength type characteristics, rebalanced quarterly in January, April, July and October.

- A backtest, from 7/6/2006 (inception of FTCS) to 5/31/2017, showed a 24.7% annualized return with a maximum drawdown of -25.7%, and low average annual turnover of about 80%.

- Over the same period the First Trust Capital Strength ETF (FTCS), which selects stocks from the NASDAQ Index, produced only 9.63% annualized return with a maximum drawdown of -53.6%.

- FTCS’s performance is not much better than that for SPY (the ETF tracking the S&P 500), which over this period returned 8.25% annualized, with a maximum drawdown of -55.2%.

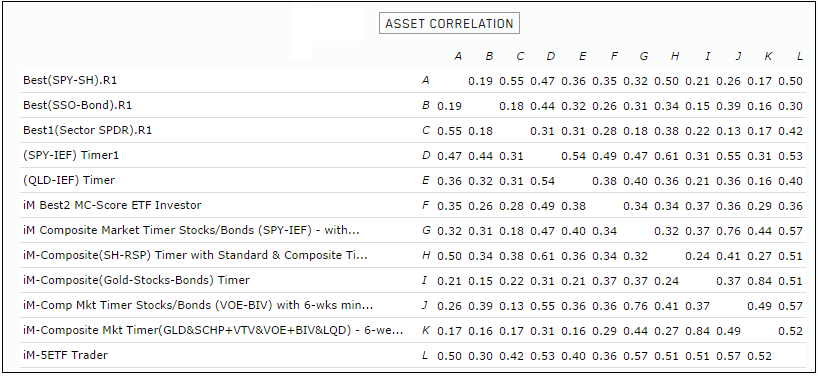

Correlation between the iM ETF Models

Currently we have 12 different ETF models at iMarketSignals. The various models and their correlation between them are shown below.

With reference to Section 202(a)(11)(D) of the Investment Advisers Act:

We are Engineers and not Investment Advisers,

read more ...

By the mere act of reading this page and navigating this site you acknowledge, agree to, and abide by the

Terms of Use / Disclaimer