- The S&P 500 averaged 6,736 for October 2025, 2,604 points above its long-term trend of 4,132, implying a 39% decline to reach the trend and signifying a valuation substantially above historic norm.

- The long-term trend indicates a forward 10-year annualized real return of only 1.4%, while the CAPE-MA35 methodology derived 10-year annualized real return is also modest at about 4.3%, indicating limited long-term upside.

- The short-term outlook indicated by CAPE-MA35 Neutral phase has historically yielded low short-term returns.

Blog Archives

Stocks Are Overvalued, Expect Losses And Low 10-Year Forward Returns: Update October 2025

The iM CAPE-MA35 ETF Rotation Strategy with 4 ETFs

- This is a dynamic ETF allocation strategy using the CAPE-MA35 ratio—the Shiller CAPE divided by its 35-year moving average—to identify market phases and adjust portfolio exposure.

- The model defines four primary phases with respective ETFs—Growth (QQQ), Defensive (GLD, XLU), Uptrend (QQQ, XLE), and Downtrend (GLD)—based on the trend and relative valuation of CAPE-MA35. ETF allocations are adjusted monthly in response to these phases.

- Backtesting from 1999 to 2025 shows the model outperforms SPY with 20.1% annualized returns, lower drawdowns, and consistent long-term performance with low turnover.

- The strategy offers a practical, rules-based approach to market timing, blending long-term valuation with trend analysis for superior risk-adjusted returns.

Dynamic ETF Allocation Using CAPE-MA35: A Market Timing Framework Based on the Shiller CAPE

- This study presents a rules-based ETF allocation model that uses the CAPE-MA35 ratio—the Shiller CAPE divided by its 35-year moving average—to identify distinct market phases and dynamically adjust portfolio exposure.

- The model defines four primary phases—Growth, Defensive, Uptrend, and Downtrend—based on the trend and relative valuation of CAPE-MA35. ETF allocations are adjusted monthly in response to these phases.

Stocks Are Still Overvalued Despite Recent Significant Declines, Expect Further Losses, But Modest 10-Year Forward Returns: Update April 2025

- The average of S&P 500 for March 2025 was 5,680, declining to 5,074 by April 4, 2025 (now 13% up from Jul-2023 average of 4,497 when forward returns for stocks “looked reasonably good” according to this analysis).

- The S&P 500 is still 1,140 points higher than the corresponding long-term trend value of 3,934 for April 2025.

- For the S&P 500 to reach the corresponding long-trend value would entail a 22% decline from the April 4, 2025 value, indicating that the S&P 500 is still considerably overvalued.

- Assuming that the current S&P 500 value remains unchanged until the end of April, then the CAPE-ratio would be 31.0, 15% higher than its 35-year moving average (MA35), currently at 26.9.

- The long-term trend indicates a forward 10-year annualized real return of 4.0%, while the CAPE-MA35 methodology derived 10-year annualized real return is better at about 6.7%.

Stocks Are Overvalued Expect Only Modest 10-Year Forward Returns: Update March 2025

- The average of S&P 500 for Mar-2025 was 5,680, (26% up from Jul-2023 average of 4,497 when forward returns for stocks “looked reasonably good” according to this analysis).

- The S&P 500 is now 1,760 points higher than the corresponding long-term trend value of 3,920.

- For the S&P 500 to reach the corresponding long-trend value would entail a 31% decline from the March average value, indicating that the S&P 500 is considerably overvalued.

- The Shiller CAPE-ratio is at 34.9, 30% higher than its 35-year moving average (MA35), currently at 26.9, forecasting a 10-year annualized real return of about 5.5% derived from the CAPE-MA35 methodology.

- The long-term trend indicates a forward 10-year annualized real return of only 2.7%

The iM Seasonal Multi-Sector Investment Strategy

- The iM Seasonal Multi-Sector Investment Strategy capitalizes on a seasonality-based approach to investing, leveraging the well-known “Sell in May and Go Away” phenomenon.

- During the winter period (end of October to the end of April) the model invests in the five highest-ranked U.S. Sector ETFs equally weighted.

- Selection is based on the performance of 30 sector ETFs during the previous one- and two-year winter periods, and not by selecting arbitrarily cyclical- and defensive categories for the winter- and summer periods.

- In the summer period the model allocates funds equally between the iShares 20+ Year Treasury Bond ETF (TLT) and Invesco QQQ.

- By combining sector rotation and hedging mechanisms for inflationary periods, this strategy offers a systematic framework for maximizing returns and managing risks.

Stocks Are Overvalued And 10-Year Forward Returns Look Poor: Update December 2024

- The average of S&P 500 for Dec-2024 was 6,011, (34% up from Jul-2023 average of 4,497 when forward returns for stocks “looked reasonably good” according to this analysis).

- The S&P 500 is now 2,135 points higher than the corresponding long-term trend value of 3,876.

- For the S&P 500 to reach the corresponding long-trend value would entail a 35% decline from the December average value, indicating that the S&P 500 is considerably overvalued.

- The Shiller CAPE-ratio is at 37.9, 42% higher than its 35-year moving average (MA35), currently at 26.7, forecasting a 10-year annualized real return of about 4.6% derived from the CAPE-MA35 methodology.

- The long-term trend indicates a forward 10-year annualized real return of only 2.0%

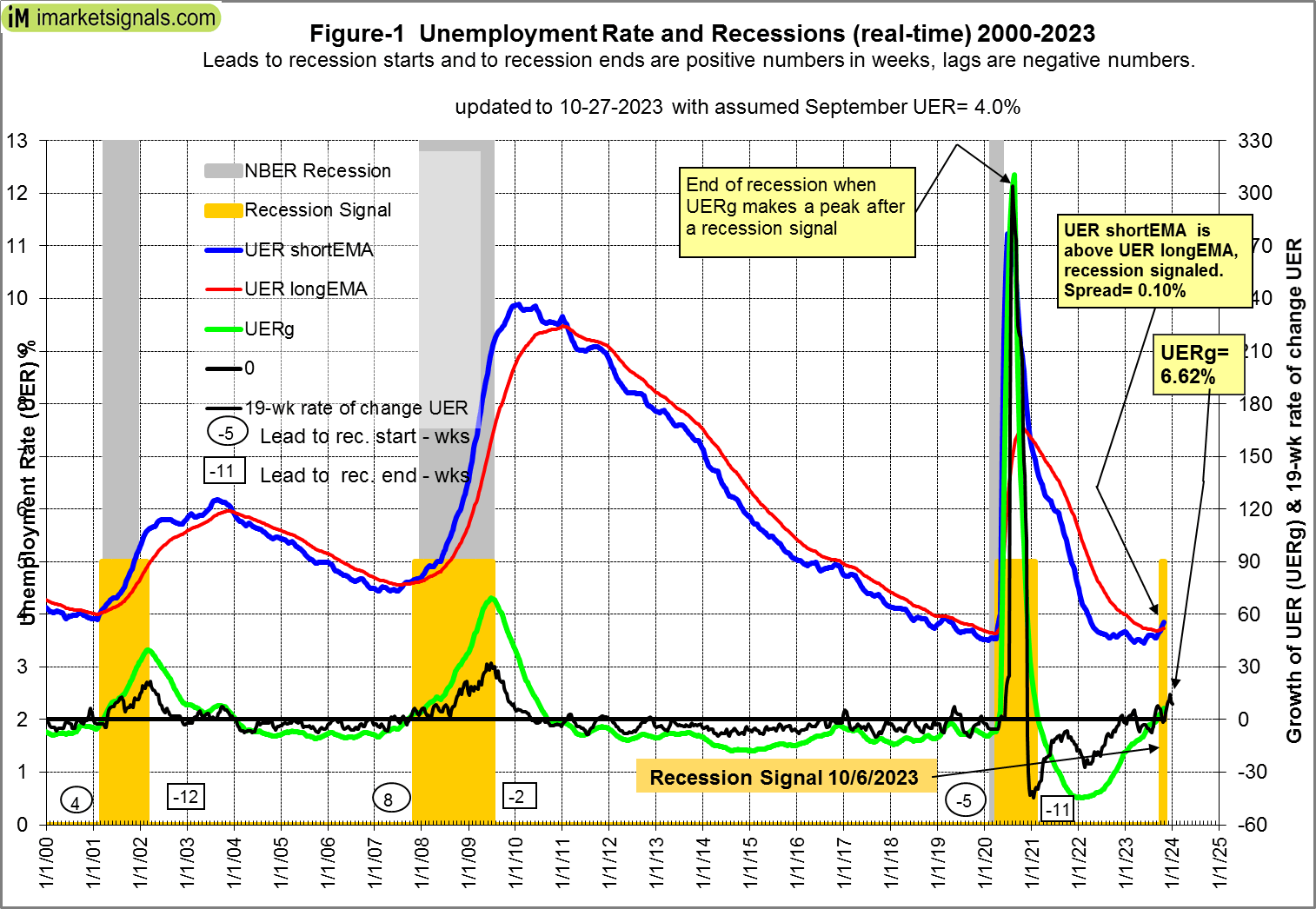

A September Unemployment Rate of 4.0% Will Signal a Recession

- A reliable source for recession forecasting is the unemployment rate (UER), which can provide signals for the beginnings and ends of recessions.

- The model was published in 2012 and has correctly signaled the 2020 recession.

- The latest UER (August 2023) is 3.8%, signifying no recession. However, if the September UER is 4% or higher a recession will be signaled according to the model.

Stocks Are Moderately Overvalued And 10-Year Forward Returns Look Reasonably Good: Update July 2023

- The average of S&P 500 for July-2023 was 4,497 (4% down from Dec-2021 high average of 4,675) and is 859 points higher than the corresponding long-term trend value of 3,638.

- For the S&P 500 to reach the corresponding long-trend value would entail a 20% decline from the July average value, indicating that the S&P 500 is moderately overvalued.

- The Shiller CAPE-ratio is at 30.9, 19% higher than its 35-year moving average (MA35), currently at 26.1, forecasting a 10-year annualized real return of about 6.5%.

- The long-term trend indicates a forward 10-year annualized real return of 4.4%

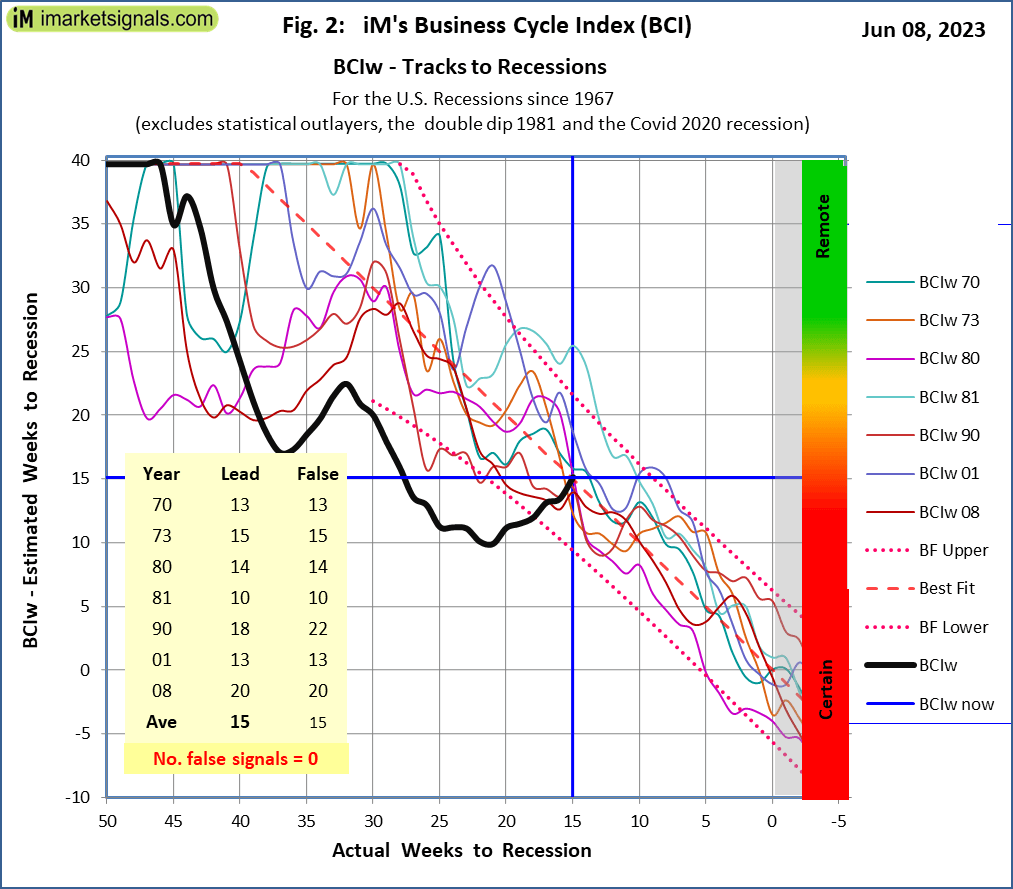

iM’s Business Cycle Index Recovers but still Signals a Recession – Update 6/9/2023

- Knowing when the U.S. economy is heading for recession is paramount to successful investment decisions.

- Our weekly Business Cycle Index would have provided early reliable warnings for the past seven recessions and signaled the Covid 2020 recession one week late.

- The BCIg has signaled a recession warning mid March 2023, but BCIg recovered and is no longer signalling a recession.

- However the BCIw, also on recovery path, continues to signal a recession which now is estimated to begin in 9 to 22 weeks.

- It is too early to say if a recession has been averted, more likely is it is delayed towards the end the end of 2023 or begin 2024.

With reference to Section 202(a)(11)(D) of the Investment Advisers Act:

We are Engineers and not Investment Advisers,

read more ...

By the mere act of reading this page and navigating this site you acknowledge, agree to, and abide by the

Terms of Use / Disclaimer