- The system screens for high dividend, low volatility S&P 500 stocks yielding significantly more than the average yield of the index and which also have a low 3-yr beta.

- Market timing rules related to our long-period backtest models, the MAC-US Timer, CAPE-Cycle-ID, and Inflation Timer have been incorporated into the model’s algorithm, and turnover has been modestly increased by introducing an additional sell signal based on volatility.

- The 16.5 year backtest of the original iM HiD-LoV-7 System produced annualized return of about 22% with a maximum drawdown of -34%, whereas the improved model provided annualized return of about 25% with a maximum drawdown of -14% over the same backtest period. (Figure-3a)

Blog Archives

Improvements to the iM HiD-LoV-7 System

Updated: Timing the Stock Market with the Inflation Rate

- Stocks usually perform poorly when inflation is on the rise. Using the inflation rate, we developed a market timer according to two simple rules.

- Switching according to the Timer signals between the S&P500 with dividends and a money-market fund would have provided from Aug-1953 to end of Jan-2016 and annualized return of 12.69%.

- Over the same period buy-and-hold of the S&P500 with dividends showed an annualized return of 10.08%, producing about a quarter of the total return of the Timer model.

The MAC-US Timer – a Moving Average Crossover System of the S&P 500

- Switching between stocks and bonds as signaled by a simple moving average crossover system of the S&P 500 – the MAC-US Timer – produces significantly higher returns than buy-and-hold stocks.

- The model has been updated from Aug-1965 to Jan-2017, conservatively assuming that funds are placed in the money market when not in the stock market.

Timing the Stock Market with the Inflation Rate

- Stocks usually perform poorly when inflation is on the rise. Using the inflation rate, we developed a market timer according to two simple rules.

- Switching according to the Timer signals between the S&P500 with dividends and a money-market fund would have provided from Aug-1953 to end of Jan-2016 and annualized return of 12.48%.

- Over the same period buy-and-hold of the S&P500 with dividends showed an annualized return of 10.08%, producing about a quarter of the total return of the Timer model.

Posted in blogs

The iM Composite Timer Gold-Stocks-Bonds

- This model uses the rules of the iM-Gold Timer and the iM-Composite Market Timer to signal periodic investments in gold, stocks and bonds.

- From Jan-2000 to Jan-2017 the Gold Timer signaled eight gold investment periods totaling only 9.3 years, while for the remaining periods totaling 7.7 years the model would have been in cash.

- During the “cash periods” the Composite Market Timer provides the signals when to invest in stock and/or bond ETFs. Bond ETFs include the ETF (XLU) are also selected according to the prevailing Market Climate Score (MC-Score) and a ranking system.

The Long Leading Recession Indicator DAGS is signaling an oncoming Recession.

On January 20, 2017, our long leading recession indicator DAGS signaled an oncoming recession.

Based on past history a recession could start at the earliest in 6 months (July-2017), but not later than 28 months from now (May-2019). The average lead time to previous recessions provided by DAGS would have been 15 months.

Forecasting Stock Market Returns with Shiller’s CAPE Ratio and its 35-Year Moving Average

- Shiller’s Cyclically Adjusted Price to Earnings Ratio (CAPE ratio) is at 27.8, which is 11.1 above its long-term mean of 16.7, signifying overvaluation of stocks and low forward returns.

- The alternative CAPE ratio methodology offered in this article references stock market valuation to a 35-year moving-average of the Shiller CAPE ratio instead of to the 1881-2016 fixed long-term mean.

- The latest CAPE ratio predicts a 10-year annualized real return of only 1.5%, whereas the presented methodology forecasts 5.8%, similar to the long-term market trend expected real return of 5.4%.

The iM Gold-Timer – Rev1

We have revised the iM Gold-Timer. The timer endeavors to signal long-term investment periods for Gold. It uses the SPDR® Gold Shares ETF: GLD. When not invested in GLD the model goes to 100% cash.

Timing the Stock Market with the Shiller CAPE

- The Shiller CAPE (cyclically adjusted price-earnings ratio) is typically regarded as a stock market valuation measure. When the CAPE is high stocks are supposed to be expensive, and vice-versa.

- The CAPE itself is not a good stock market timer. However, the CAPE can indirectly be used for market timing by determining a Cycle-ID as formulated by Theodore Wong.

- Our 1950-2016 backtest of the CAPE-Cycle-ID model, when switching between the S&P500 with dividends and the money market, showed an annualized return of 11.9%, versus 10.4% for buy-and-hold.

On Track for 2.5% Inflation by December 2016; Update November 2016.

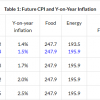

- On September 19, we estimated an inflation rate of 2.5% for December 2016, and 1.4% for September 2016.

- Actual September inflation came in at 1.5%, the December inflation estimate remains at 2.5%.

- With inflation rising, and markets uncertain, Treasury Inflation Protected funds (TIPS) should remain a reasonably safe investment. Conventional bond funds are expected to perform worse than TIPS funds.

Posted in blogs

With reference to Section 202(a)(11)(D) of the Investment Advisers Act:

We are Engineers and not Investment Advisers,

read more ...

By the mere act of reading this page and navigating this site you acknowledge, agree to, and abide by the

Terms of Use / Disclaimer