- An investor who is able to assess stock market climate, and able to adjust asset allocation accordingly, will have an advantage in the market.

- Four different approaches are used to assess market climate which are based on economic, momentum and sentiment indicators. This results in five different market climate segments.

- During up-markets the system is invested in long equity ETFs and then switches progressively to fixed-income ETFs when neutral or negative stock market climates exist.

- This system invests simultaneously in four Vanguard ETFs (or their corresponding mutual funds), appropriately selected for the prevailing market climate, and typically holds them for longer than a year.

- A backtest of the model from Jan-2000 to Aug-2016 shows an average annual return of 15.0% with a maximum drawdown of -12.6% and a low average annual turnover of 92%.

A month ago we introduced a system holding two ETFs depending on the market climate. The model described in this article uses the same system and selects, according to market climate four Vanguard ETFs (or their corresponding mutual funds) which can be bought commission free at Vanguard. It is intended for savers who have control over asset allocations in their retirement accounts.

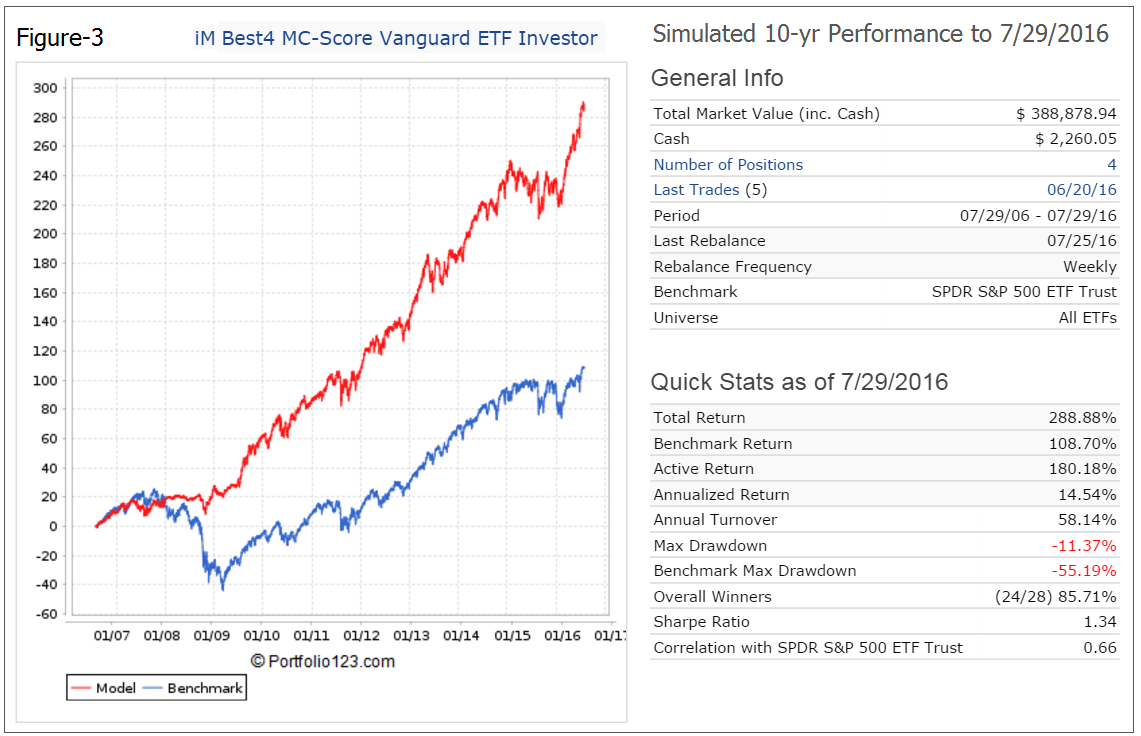

Pension fund contributions are typically directed to the default investment option of Target Date Funds, also known as Lifecycle Funds, or Freedom Funds, if no investment instruction is provided by employees. Unfortunately for savers the returns from these funds have been rather disappointing. On average the 10-year average annual total return to 7/29/2016 was 5.94% for the Vanguard Target Date Funds, 5.61% for the TIAA-CREF Lifecycle Funds, and 4.94% for the Fidelity Freedom Funds. (Over the same period the iM MC-Score Vanguard ETF Investor model shows a simulated 14.5% average annual return. See Figure-3 in the Appendix.)

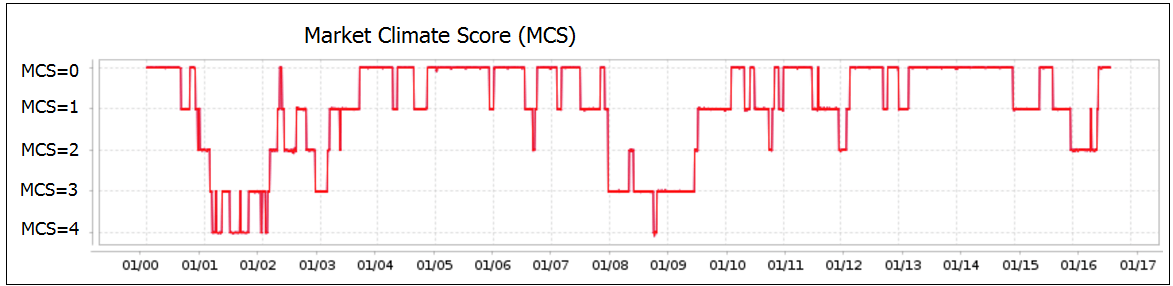

Investors and savers can do better by changing investment allocation according to market climate. This does not involve frequent trading as there were relatively few changes of the Market Climate Score (MCS) from Jan-2000 to Aug-2016, as shown on the chart below. Periods of market weakness are defined by market climate scores MCS=3 and MCS=4 when equity funds are avoided.

Over the longer term, this simple strategy described here should always provide higher returns than buy-and-hold, and perform better than most managed or index funds.

The 10-ETF Vanguard Selection List:

The system selects from the five equity ETFs and the five fixed-income ETFs listed below:

VAW Vanguard Materials ETF

VDC Vanguard Consumer Staples ETF

VNQ Vanguard REIT ETF

VOE Vanguard Mid-Cap Value ETF

VPU Vanguard Utilities ETF

BIV Vanguard Intermediate-Term Bond ETF

BSV Vanguard Short-Term Bond ETF

VGIT Vanguard Intermediate-Term Government Bond ETF

VMBS Vanguard Mortgage-Backed Securities ETF

VWOB Vanguard Emerging Markets Government Bond ETF

Notes:

- The model was backtested using the on-line portfolio simulation platform Portfolio 123, which also provides extended price data for ETFs prior to their inception dates calculated from their proxies.

- Prior to the inception dates of the ETFs VAW, VDC, VPU and VGIT the following ETFs were used XLB, XLP, XLU and IEF, respectively.

Market climate measurement:

The system described herewith relies on the following economic indicators:

- Russell 1000 Index.

- S&P 500 earnings per share estimate (SPEE), based on the time weighted analyst’s estimates of current year and next year.

- Short Interest Percent of Float for the S&P 500 (SPSI).

- The Aggregate Spread, similar to the Enhanced Aggregate Spread, is a recession indicator with a long lead time, which uses:

- 20-year US Treasury bond yield (Y20),

- Target Federal Funds Rate (FFR),

- Consumer Price Index (CPI),

- Unemployment Rate (UER).

- The Hi-Lo Index of the S&P 500 measures the excess of the number of shares reaching new 3-month highs versus the number of shares forming new 3-month lows.

These five indicators are used in four climate models which indicate a weak market climate when:

- The unemployment rate is on the increase: UER now > UER 3-mo ago.

- The earnings estimate of the S&P500 declines: SPEE now < SPEE 20-wks ago.

- The short moving Average (MA) < long MA of the Russell 1000 Index.

- The three following conditions are true

- (Aggregate Spread 10-mo ago < 150 bps) and

- (short MA < long MA of the Hi-Lo Index) and

- (short MA > long MA of SPSI).

The iM Market Climate Score System:

The MC-Score is assessed by summing the four climate models’ scores (score is 1 when measure is true, or 0 when false). In each market segment the investment style is altered; this model invest in four ETFs (equal dollar weighted) as tabled below:

| MC-Score | Climate | Vanguard ETF’s Selected | |||

| 0 | Best | VDC | VPU | VNQ | VOE |

| 1 | Positive | VDC | VPU | VNQ | VWOB |

| 2 | Neutral | VAW | VNQ | BIV | VWOB |

| 3 | Negative | VGIT | VMBS | BIV | VWOB |

| 4 | Worst | BSV | VMBS | BIV | VWOB |

Note, that the overlap of ETF symbols with MC-Score groups, which significantly reduces trading.

Trading:

The model is rebalanced weekly, so that market climate score changes can be acted upon. ETFs are bought and sold at the closing price on the first trading day of the week after the same market climate change signal has been generated twice in succession; i.e. for the current week and the previous week. Transaction slippage and brokerage fees were neglected because the model uses closing prices, and Vanguard ETFs can be traded free of brokerage fees at Vanguard.

The only buy rule specifies the four ETFs for each of the five MC-Score groups. There is only one sell rule to ensure that ETFs are held at least two weeks and are only sold when the market climate score changes from the previous week. There is no need for a ranking system because the model only selects the four ETFs specified for each market climate score.

Historic performance of the iM MC-Score Vanguard ETF Investor System:

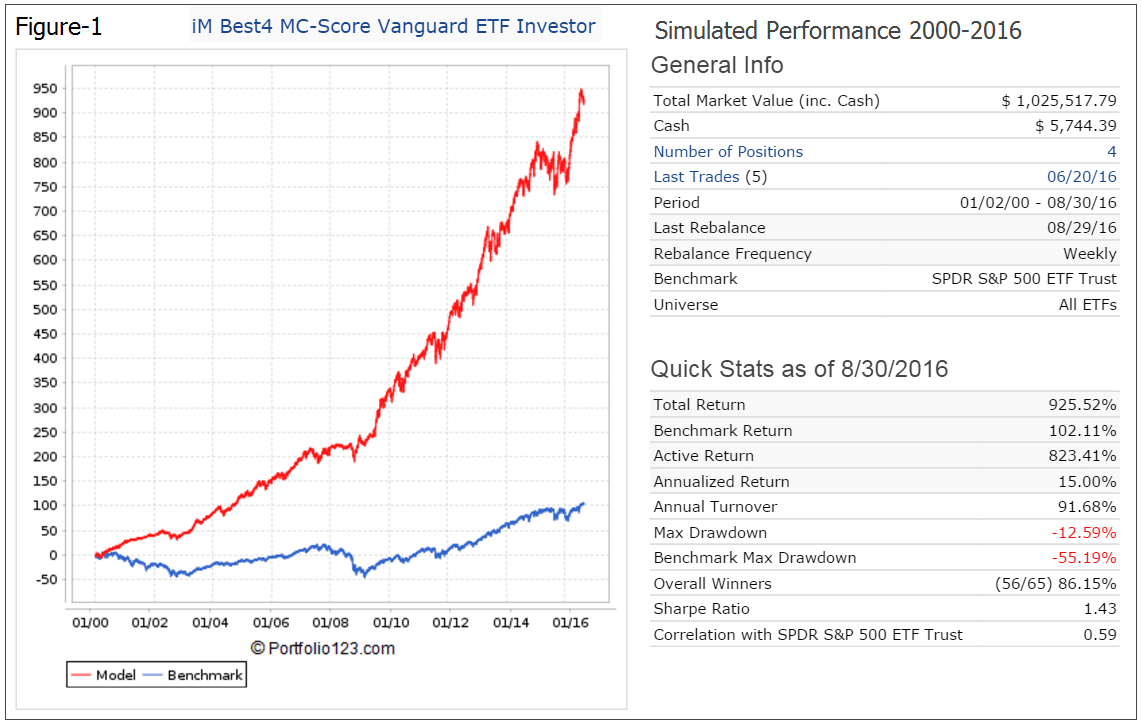

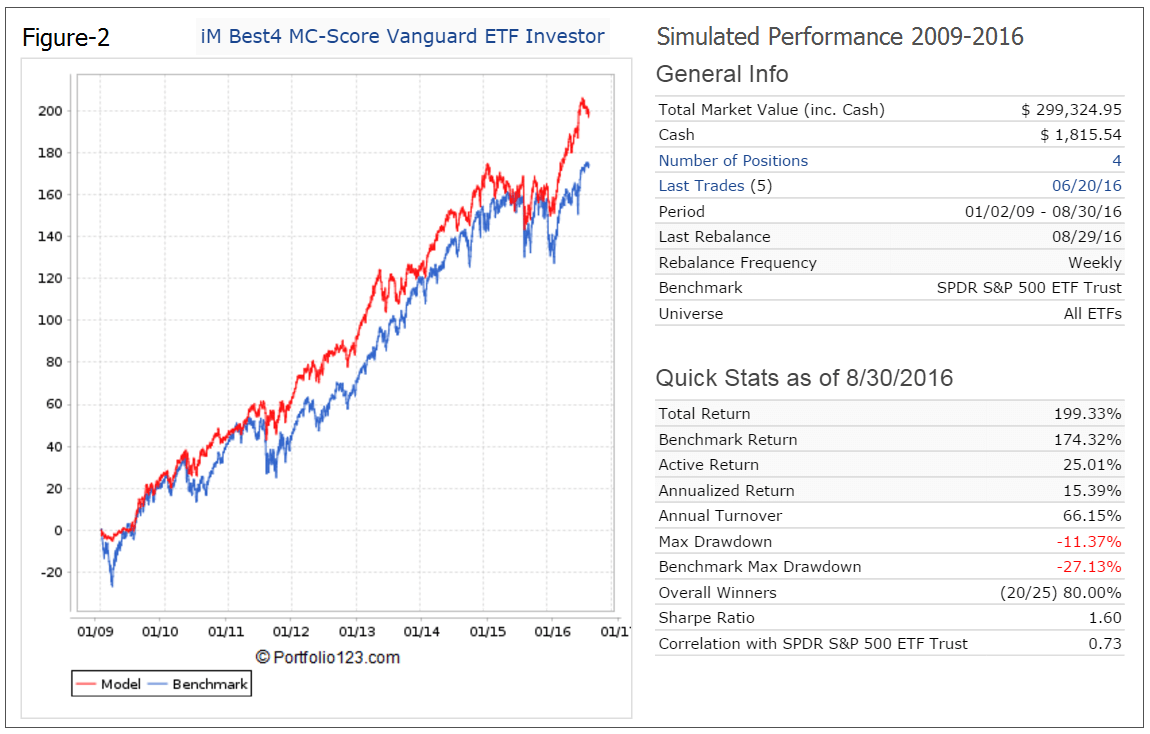

In the Figures-1 and 2 the red graph represents the model and the blue graph shows the performance of benchmark SPDR S&P 500 ETF Trust ETF (SPY).

Figure-1: Simulated Performance 2000-2016: Annualized Return= 15.0%, Max DD= -12.6%. The backtest period was from Jan-2000 to Aug-2016. End of August holdings are for MCS= 0: VDC, VPU, VNQ, VOE. Also, the model currently holds $5,744 in cash. Figure-2: Simulated Performance 2009-2016: Annualized Return= 15.4%, Max DD= -11.4%. The backtest period was from Jan-2009 to Aug-2016. During this general up-market period the model matched the performance of SPY, but Max DD was significantly better.

Following the Model:

The backtests confirm that a successful strategy would be to invest in ETFs having styles that are applicable to prevailing market climate as defined by the Market Climate Score System.

This model can be followed live at iMarketSignals, where it will be updated weekly.

Appendix

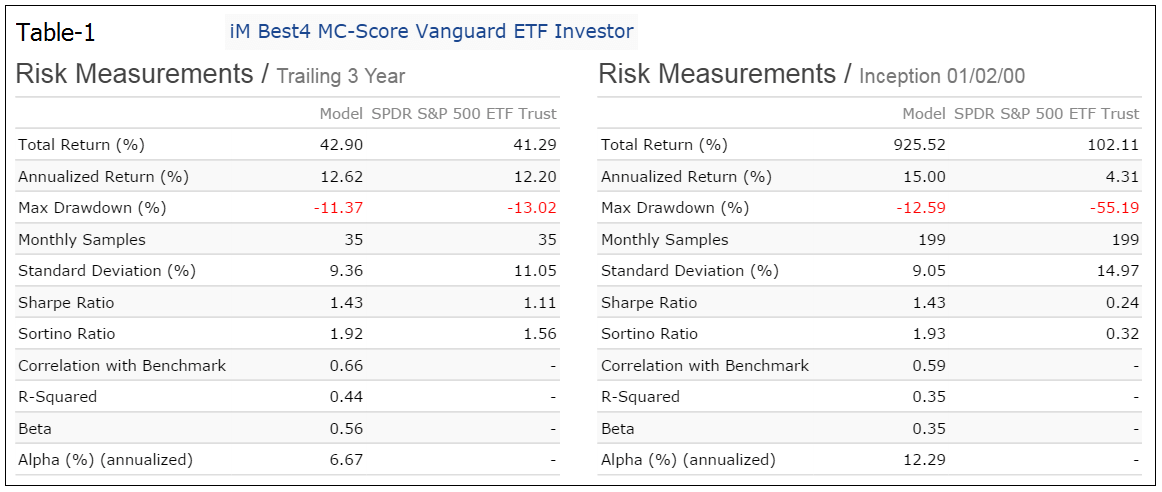

Risk Measurements:

Table-1 lists the annualized returns, maximum drawdown, and various risk measurements for the trailing three years and for the full backtest period.

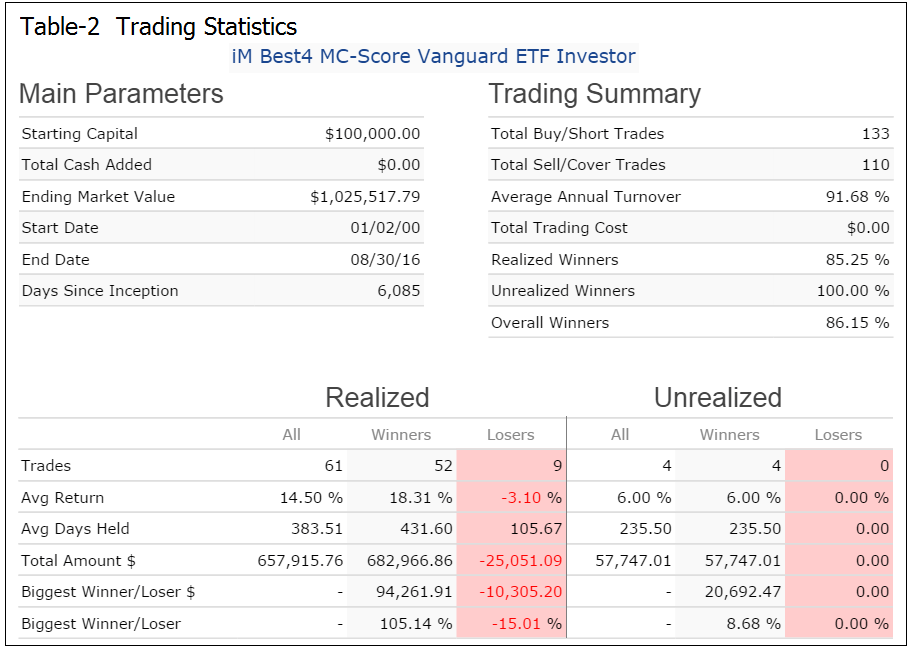

Trading Statistics:

Table-2: Note that the total amount of all Realized Losers is only about 4% of the total amount of all Realized Winners. This model had a high win rate of 86% of all trades.

The average holding period for all Realized Trades was 383 days, and so far the current holdings have been held for 235 days.

There were 110 Total Sell Trades of which 61 were Realized Trades when the market climate score changed. The balance of 49 completed trades accounts for small rebalance trades to take account of dividends received and adjusting holdings to equal weight. Moreover, there were 133 Total Buy Trades, but only 110 Total Sell Trades. Since the model holds four positions, there were 133-110-4=19 Buy Trades incorporated into other subsequent Sell Trades.

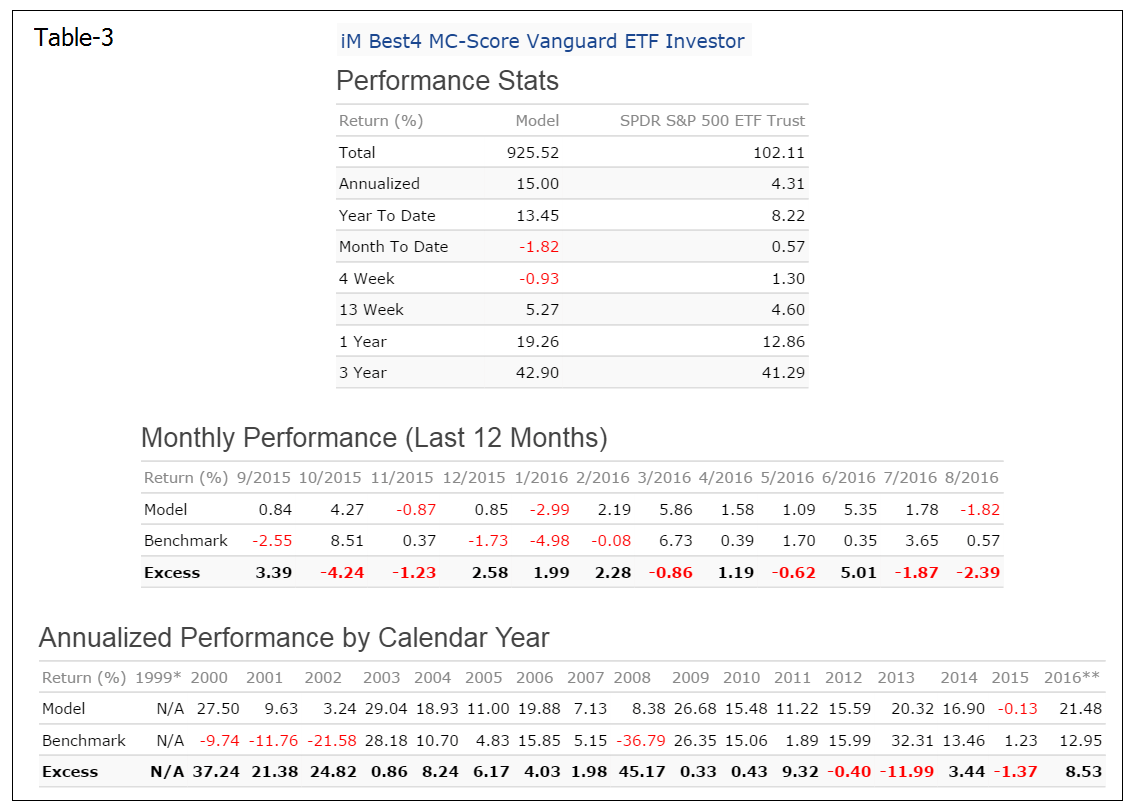

Performance Statistics:

Figure-3: Simulated 10-yr Performance to 7/29/2016: Annualized Return= 14.5%, Max DD= -11.4, and low average Annual Turnover of 58%. This can be directly compared with the 10-yr performance of the Target Date Funds.

Disclaimer:

One should be aware that all results shown for the Market Climate Score System are from a simulation and not from actual trading.

All information for this model is back-tested, based on the methodology that was in effect on the launch date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of a methodology and selection criteria in hindsight. Actual returns may differ from, and be lower than, back-tested returns.

All results are presented for informational and educational purposes only and shall not be construed as advice to invest in any assets. Backtesting results should be interpreted in light of differences between simulated performance and actual trading, and an understanding that past performance is no guarantee of future results. All investors should make investment choices based upon their own analysis of the asset, its expected returns and risks, or consult a financial adviser.

Hi Anton and Georg

I like this strategy. But for the folks here that are not concerned about trading, might there be a better set of ETFs for the Selection List, other than the one’s suggested here, that would return a higher Sharp/Sortino ratio?

If so (or even if not), might the ETFs suggested for each MC climate change?

Many thanks,

Vman

Yes, there are other ETFs which would provide a higher return than those from Vanguard. We chose the Vanguard ETFs because they are also available as mutual funds.

What is the difference in the 4 Market Climate Zones (1 through 4) and the 5 Market Climate Score (0 through 4)? Do both use the same grader? Where can I get the actual dates the MC Score changed since back-testing dates began? Thanks, Kevin

The Market Climate Score comes directly from the the four market climate measurements. Score 1 when a measure is true, or 0 when false. Then by summing one obtains the MC-Score. Since there are four market climate measurements, there are five possible scores: 0, 1, 2, 3, and 4.

How were the equity ETFs chosen? thanks

just to clarify my question, how did you decide to include these specific vanguard ETFs to represent good market conditions (as opposed to other sectors)?

Hello other than Portfolio123, are there any websites I can go to to check whether SPEE now < SPEE 20-wks ago?

What is symbol SPEE representing?

S&P 500 earnings per share estimate (SPEE), based on the time weighted analyst’s estimates of current year and next year.