The iM-Best(SPY-IEF) MarketTimer incorporates three market timing models which provide signals which indicate the percentage of funds to allocate to stock market investment in 25% increments, from 0% to 100%, also referred to as signal strength.

Alternatively, instead of allocating a percentage of funds to stocks and bonds, one can be fully invested in stocks or bond funds according to the signal strength, as shown in the tables below.

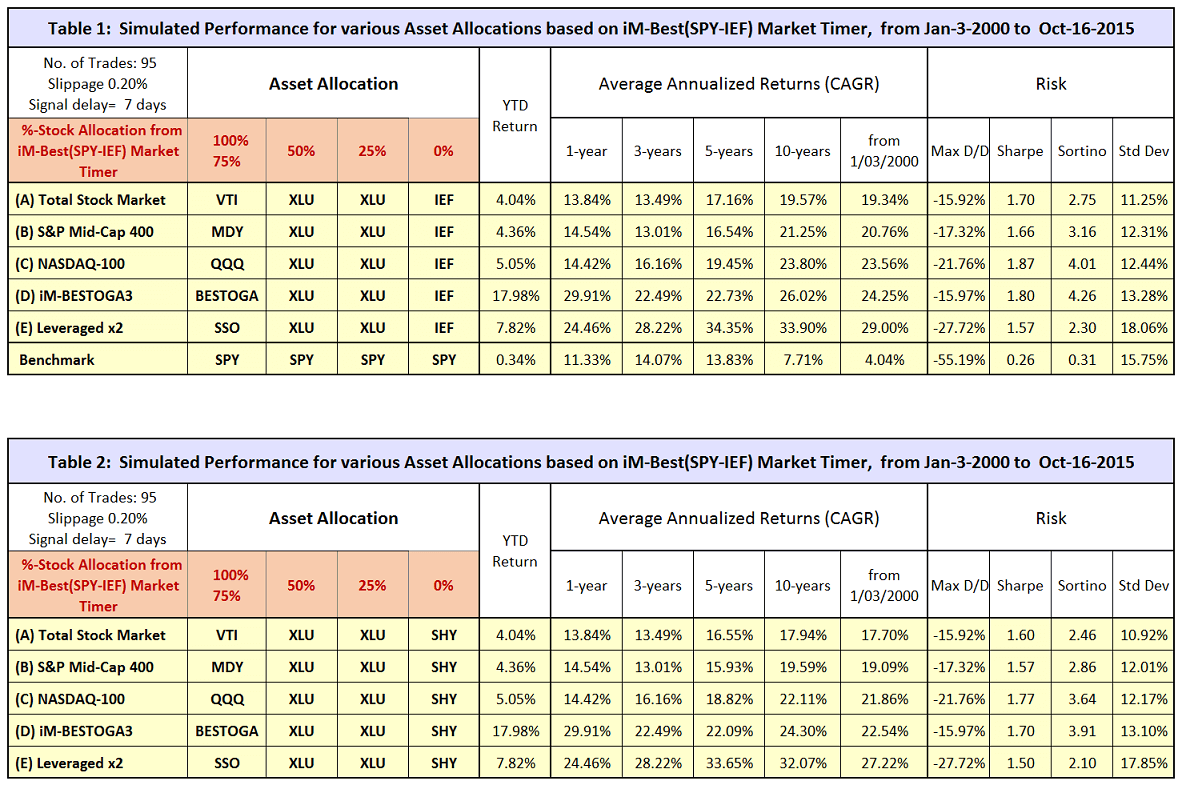

Performance is shown for the following asset allocations:

- When the Timer signal strength is 100% or 75% the model invest 100% of funds in a stock ETF such as VTI, MDY, or QQQ. (A stock trading model such as BESTOGA3, or the 2x leveraged SSO, can be used as well.)

- When the Timer signal strength is 50% or 25% the model invest 100% of funds in the Utilities Select Sector SPDR® Fund (XLU)

- When the Timer signal strength is 0% the model invests 100% of funds in a bond ETF such as IEF, or SHY.

The above performance figures assume closing prices adjusted for dividends and incorporate transaction cost of 0.2% for each switch trade to allow for brokerage fees and slippage. Also trade execution was delayed by 7 days after a signal to ensure that time between trades was longer than 7 days. This resulted in 95 completed trades over the backtest period.

For all asset allocations performance and risk measurements are superior to those of the benchmark SPY, the ETF tracking the S&P500.

Disclaimer

One should be aware that most of the results shown are from a simulation and not from actual trading. Out-of-sample performance of the Timer’s three component models is relatively short, about 2 years. This timing model is presented for informational and educational purposes only and shall not be construed as advice to invest in any assets. Out-of-sample performance may be much different. Backtesting results should be interpreted in light of differences between simulated performance and actual trading, and an understanding that past performance is no guarantee of future results. All investors should make investment choices based upon their own analysis of the asset, its expected returns and risks, or consult a financial adviser.

Have you looked at how VMNFX (market neutral, long and short in market sectors) might work as an alternative to XLU, IEF, and/or SHY in this and perhaps others of your timing strategies? Just eyeballing the charts, it looks like it might be able to provide some protection against crashes and the seemingly increased risk of correlation between stocks and bonds these days, while doing better than cash. With its unusual approach to market neutrality, it doesn’t correlate very highly with most of the standard broad indices.

According to Vanguard’s website the minimum investment in VMNFX is $250,000. We will look to see how this fund could fit into an asset allocation strategy for the Timer.

You do have to open the position at 250K, but then you can reduce it to a lower amount to fit a timing strategy. If you leave a little in to keep the position open, I don’t think they close you out. Interested to see if you come up with something. I’m impressed by your work generally.

Placing VMNFX into Zone-3 or Zone-4 slots produced lower returns with higher max D/D than having XLU and IEF in those slots.

Thanks. Your willingness to check things like this is unusual and much appreciated.

In response to a question on the original blog post on SPY-IEF, you indicated that the correlation with COMBO3 was around 0.70. Is that still the case after the changes to full investment and different ETF’s in this alternative version? Which changes result in lower correlations with COMBO3? (I have both in action at this point.)

Also, it would be helpful to me and probably others to receive a detailed weekly update data table on at least the basic SPY-IEF system, like those you provide for COMBO3 and most other systems. An occasional frequent update on these new alternative strategies would also be useful.

The SPY-IEF Timer model has a correlation of about 0.70 with Combo3 as originally posted. The correlation is determined over the length of the backtest period and would not change much due to a recent signal change of the Timer.

We have not checked correlation to Combo3 if ETFs other than SPY and IEF are used.

We will consider posting weekly performance updates for the Timer.

Thanks. And best for the holidays.

George,

Since most people in 401ks do not have XLU available would be so kind as to test another variant:

100-75% VTI 100%, 50% VTI 50%, 25% VTI 25%, 0% SHY 100%

complete with max dd and sharpe

For your asset allocation simulated performance (CAGR) to Dec-4-2015 is as follows which includes slippage of 0.1% of each buy and sell trade:

YTD= 2.74%

1yr= 2.60%

3yrs= 16.28%

5yrs= 14.22%

10yrs= 14.03%

from Jan-2000= 13.04%

max D/D= -18.54

Sharpe= 1.14

Sortino= 1.52

Std Dev= 11.30%

George,

Since most people in 401ks do not have XLU available would be so kind as to test another variant:

100-75% VTI 100%, 50%-25% CONSERVATIVE ALLOCATION FUND, 0% SHY 100%

complete with max dd and sharpe

Which CONSERVATIVE ALLOCATION FUND?

In my case would be Wellsley – VWINX or VWELX.

Tx

Sorry, delete VWELX

You obviously are using Vanguard Mutual Funds.

For Mutual Funds there is no slippage or commission payable.

allocation for

signal strength 100-75%: VFINX

signal strength 50%: VWINX

signal strength 25%: VWINX

signal strength 0%: VBISX

Simulated Performance Jan-2000 – Dec-4-2015:

YTD= 5.84%

1yr= 5.31%

3yrs= 16.36%

5yrs= 17.18%

10yrs= 16.59%

from Jan-2000= 14.89%

max D/D= -14.48

Sharpe= 1.62

Sortino= 2.22

Std Dev= 9.10%

But a good allocation would also be:

signal strength 100-75%: VFINX (stocks only)

signal strength 50%: VWELX (2/3 stocks, 1/3 bonds)

signal strength 25%: VWINX (1/3 stocks, 2/3 bonds)

signal strength 0%: VBISX (short-term bond fund)

Simulated Performance Jan-2000 – Dec-4-2015:

YTD= 5.86%

1yr= 5.32%

3yrs= 16.29%

5yrs= 15.63%

10yrs= 16.86%

from Jan-2000= 15.62%

max D/D= -17.18

Sharpe= 1.67

Sortino= 2.29

Std Dev= 9.28%

Thanks George,, results better than I thought! Hopefully this helps a lot of your readers.

The only problem using Vanguard mutual funds is the restriction period of 60 days after having sold before one can re-enter the fund again. So one should have an alternative fund ready to invest in if a signal occurs requiring re-entry before the 60 days are over. For example, one can interchange VFINX with VTSMX without there being a significant difference in returns.

I hate mutual funds. Better to use ETF’s

Georg,

This is similar to the one above but do you mind running it for me.

100-75% VTI 100% invested, 50% VTI 75% invested, 25% VTI 50% invested, 0% SHY 100%.

Thanks

This model does not allow for partial investments. i.e. 75% and 50% of VTI and remainder in cash is not possible.

By the way, how would this compare to the MAC system?

SPY-IEF with MAC algo

Simulated Performance Jan-2000 – Dec-4-2015:

CAGR= 15.62%

max D/D= -17.10

Sharpe= 0.85

Sortino= 1.21

Std Dev= 10.35%

So using the Market Timer with various asset allocations produces higher returns.

Georg,

Curious what the Timer look like under the following scenarios:

Timer 100% – SSO

Timer 75/25, 50/50, 25/75, using SPY/IEF in those proportions

Timer 0% – SH

Tom C

Also, what is the correlation of the Aggressive Market Timer you discuss in this article to the Aggressive version of the Market Climate grader?

Thanks,

Tom C

by aggressive, meaning the model for both that uses SSO.

George,

If following this model should one not act on front page dashboard signals produced by SPY/IEF unless the signal is reaffirmed at 7 days? If the answer is yes, how many basic SPY/IEF as shown on home page dashboard could be erroneous?

There are no erroneous signals listed for the Best(SPY-IEF)Market Timer.

If you wanted to trade ETFs according to it, you need to wait one week to see whether the signal stays in place before acting on it.

We are not providing ETF trading signals for the Timer, they are only provided for the Market Climate Grader.

George, Please confirm if this is correct.

SPY/IEF dashboard signals

10/26/15 50%

11/2 50% Buy XLU

11/9 50%

11/16 25%

11/23 75%

11/30 75% Buy VTI

Above action days are 11/2 and 11/30 only? No action 10/26,11/9,11/16,11/23.

Please see our comment above.

Georg,

Is it possible to estimate the correlation for the Mkt Timer “Aggressive” simulation you ran vs. the Mkt Climate Grader “Aggressive” simulation you ran when you rolled that out? Thanks.

The performance calculation for the Timer and Grader with Agressive allocations are not done on the P123 platform. We don’t calculate a performance curve for those two models which we could compare for correlation. We only calculate returns over various periods based on the trades.

Can you isolate the performance at 100% SPY (CAGR / DD / Sharpe), if we went SSO at 100% SPY in the timer, and cash at every other allocation? Thanks.

Tom C

Performance from Jan-2000 to end of Dec-2015 if we went SSO at 75% and 100% SPY in the timer, and cash at 50%, 25%, and 0% SPY allocation (our model places 75% and 100% SPY allocation into the top zone):

Annualized Returns

SSO + CASH + CASH + CASH ………………SPY

12/31/1999 … 12/31/2015 … 19.66% … 4.04%

12/31/2005 … 12/31/2015 … 27.62% … 7.23%

12/31/2010 … 12/31/2015 … 30.54% … 12.42%

12/31/2012 … 12/31/2015 … 26.48% … 14.97%

12/31/2014 … 12/31/2015 …. 7.72% ….. 1.23%

Max D/D … Sharpe … Sortino … Std Dev

-29.61% … 1.10 … 1.22 … 17.72%

Thanks. Is there any significant difference between 100 and 75 signal? Was considering pushing up to 3x for a 100% signal vs 2x for 75.

Also, is there positive expectancy in going short at the 0% signal?

Tom C

The reason we combined the 75% and 100% SPY allocations into one slot is that there was no significant difference in the future win-rate for those two allocations.

Going short at the 0% signal with SH does not improve returns significantly.

Would you please update this model’s performance (table1 and table2) from Jan-3-2000 to May-31-2016 when it gets to the end of this month.

thank you

Hey Georg,

How has this model been performing lately?

Would you please update performance to 6/30/16 for Table 1(A) Total Stock Market. We are considering using this portfolio for its combination of higher returns, lower Max D/D’s, better Sharpe and fewer trades when compared to iM-MCGrader(ETF-Model) Basic and Conservative and iM-Best(SPY-IEF) Market Timer model.

We were wondering has this outperformance continued thru 6/30/16?

Thank you