About two years ago I offered evidence that a major bull market may have commenced in 2009 (Appendix A). Additionally, a statistical analysis of the historic data of the S&P Composite presented in an Aug-2012 article and Jan-2014 update thereto supported this finding. Since August 2012 the S&P500 has now gained a real 40% to the end of June 2014. So what further gains can we expect, if any?

Will the bull market continue?

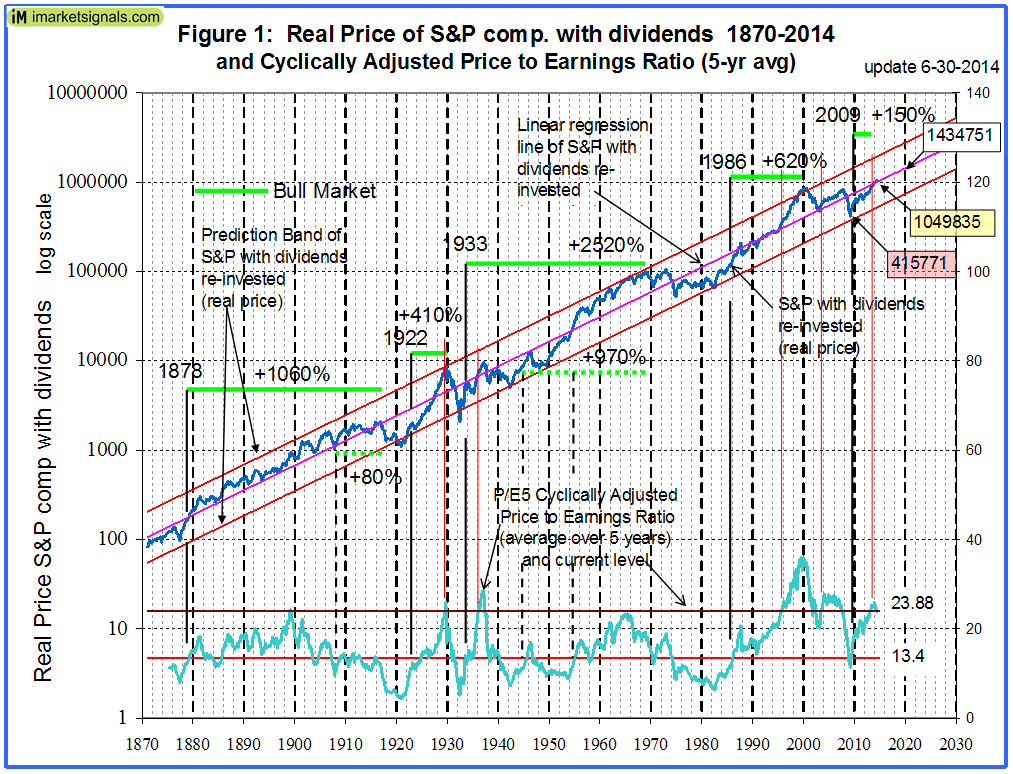

Nobody knows, and the best we can do is to use the historic data (which is from Shiller’s S&P series) to guide us to make estimates for the future. From the real price of the S&P-Composite with dividends re-invested (S&P-real) one finds that the best fit line from January 1871 onward is a straight line when plotted to a semi-log scale. There is no reason to believe that this long-term trend of S&P-real will be interrupted. S&P-real and the best fit line together with its prediction band are shown in Figure-1, updated to Jun-2014. (See appendix B for the equations.)

Also shown is the Cyclically Adjusted Price to Earnings Ratio P/E5 (which is the real price of the S&P divided by the average of the real earnings over the preceding 5 years), it is currently at a level of 23.9, down from Jan-2014 level of 26.1.

One observes that whenever S&P-real “bounced-off” the lower extreme of the prediction band and P/E5 moved from below to above 13.4 a bull market always followed. The last time this occurred was in March 2009. Since then S&P-real has “only” gained about 150%. Comparing this to previous post-bounce-off-gains (which ranged from 300% to 1720%) then the possibility exists of further gains to come.

What gains (if any) can we expect?

Extending the best fit line and the prediction band to 2020 provides a glimpse into the future which enables us to estimate the change of S&P-real from the current level of about 1,049,835. In 2020, the value of S&P-real as indicated by the best fit line is about 1,430,000, while the lowest and highest values shown by the prediction band are 740,000 and 2,770,000, respectively.

Thus the historic trend forecasts a probable gain of about 35% for S&P-real over the next five years. The worst scenario would be a possible loss of about 30%, and the best outcome would be a 160% increase.

What other analysts expect

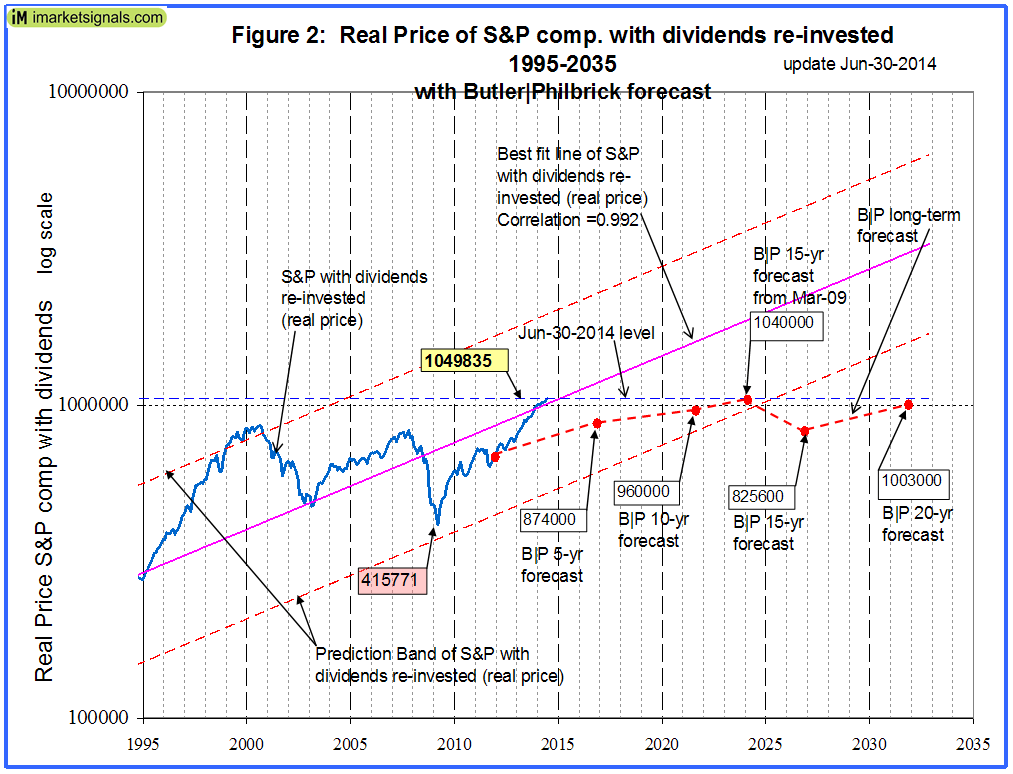

Commentators, such as Butler|Philbrick and Hussman warned us in December 2011 that the markets then were expensive and overbought, and that one could only expect very low returns going forward over periods as long as 20 years. Figure-2 shows the current situation in more detail and also includes the levels of S&P-real as per Butler|Philbrick (B|P) forecast, indicated by the red markers connected by the dashed red line.

From December 2011 onward B|P predicted a real annual return for the stock market of only 1.46% for 15 years, and 2.08% for 20 years (Table-1 in their article and Appendix C below). Also they forecasted a 6.48% annual return from Mar-2009 to Mar-2024 (Table 2 in their article). One can see that the March 2024 level is quite possible as it is just above the lower extreme of the prediction band, but it would appear that the December 2026 and 2031 forecasts are overly pessimistic.

One can see from Figure-2 that the current level of SP-real is already higher than all the forecast levels. This shows that long-term forecasts are unreliable and it would be better for financial experts to predict a range for returns than absolute values. However, the forecasts should not be discarded lightly.

Is the market overvalued?

One observes from Figure-1 that presently S&P-real is where it should be; its level still borders on its long-time historic trend line.

The P/E5 is at a high level of 23.9 but it is lower than the Jan-2014 level of 26.1. The relatively high level may indicate an overvalued market, and the graph of P/E5 has also now a downward slope. Similar conditions prevailed only 4-times in the past: in 1929, 1937, 2002 and 2008. Only after one occasion, in 2002, was it followed by a continuous market advance. however, at that time the S&P-real had been declining for several years from the upper extreme of its prediction band. At the three other occasions the S&P-real had previously peaked, and the market continued to decline for several years thereafter.

Long-term investors should also heed Shiller’s Dec-2013 warning, and consider the high level of the Shiller P/E10 ratio, currently at 26.5. He states that the plot of P/E10 “confirms that ……Long-term investors would be well advised, individually, to lower their exposure to the stock market when it is high, ….., and get into the market when it is low.” The plot shows that for a P/E10 of 25 one can expect a 10-year annualized return of between -5% and +5%. So caution is certainly indicated and one should consider market-timing models, such as the ones listed in Appendix D, to time one’s exposure to the stock market.

.png){kind=link}

Appendix A

Previous articles in support of a bull market:

- Estimating Stock Market Returns to 2020 and Beyond: Update January 2014

- Estimating Stock Market Returns to 2020 and Beyond

- Is the Next Great Bull Market Already Here?

- Get Ready for the Next Great Bull Market

- Anticipating the Ultimate Death Cross

- The Ultimate Death Cross – False Harbinger of Doom

Appendix B

The best fit line and prediction band were calculated using statistical software from PSI-Plot. There were 1699 data points from Jan-1871 to July-2012. The SP-real values for the period after July-2012 are “out of sample” and were not included in the regression analysis.

The equation of the best fit line is y = 10(ax+b) .

y = is the dependent variable of the best fit line.

x = are the number of months from January 1871 onwards.

a = 0.0023112648

b = 2.02423522

The Pearson correlation coefficient is 0.992. This number is most appropriately applied to linear regression as an indication of how closely the two variables approximate a linear relationship to each other. A perfect fit would have a correlation coefficient of 1.000.

The equation of the upper and lower extremes of the prediction band is y = 10(ax+b) , with parameters ‘y’, ‘x’, and ‘a’ as before, but with

b = 2.31005634 for the upper extreme line, and

b = 1.73841411 for the lower extreme line of the prediction band.

Appendix C

Butler|Philbrick real returns forecast for the stock market from December 2011.

Appendix D

Market-timing models periodically updated at imarketsignals.com:

- IBH – Improving on Buy and Hold: Asset Allocation using Economic Indicators

- The Improved MAC-System

- iM-Best(SPY-SH) Market Timing System: Gains for Up and Down Markets

- A Modified Coppock Indicator for the S&P500

- COMP-IBH – The Use of Recession Indicators in Stock Market Timing

- Exit Signals for the Stock Market from iM’s Business Cycle Index

Strong Work! Very impressive. Now, this doesn’t rule out an event like 1987 correction, right?

This analysis does not provide guidance to market corrections – it is a long range forecast of possible real value of the S&P adjusted for dividends. On Figure-1 one can see the 1987 correction and the subsequent bull-market to 2000.

Exactly, this is exactly why I asked. There is a lot of talk how 2014 is similar to 1987 and your chart shows it too.

Good observation. I will provide a chart from 1970 onward, so we can see the similarities between then an now.