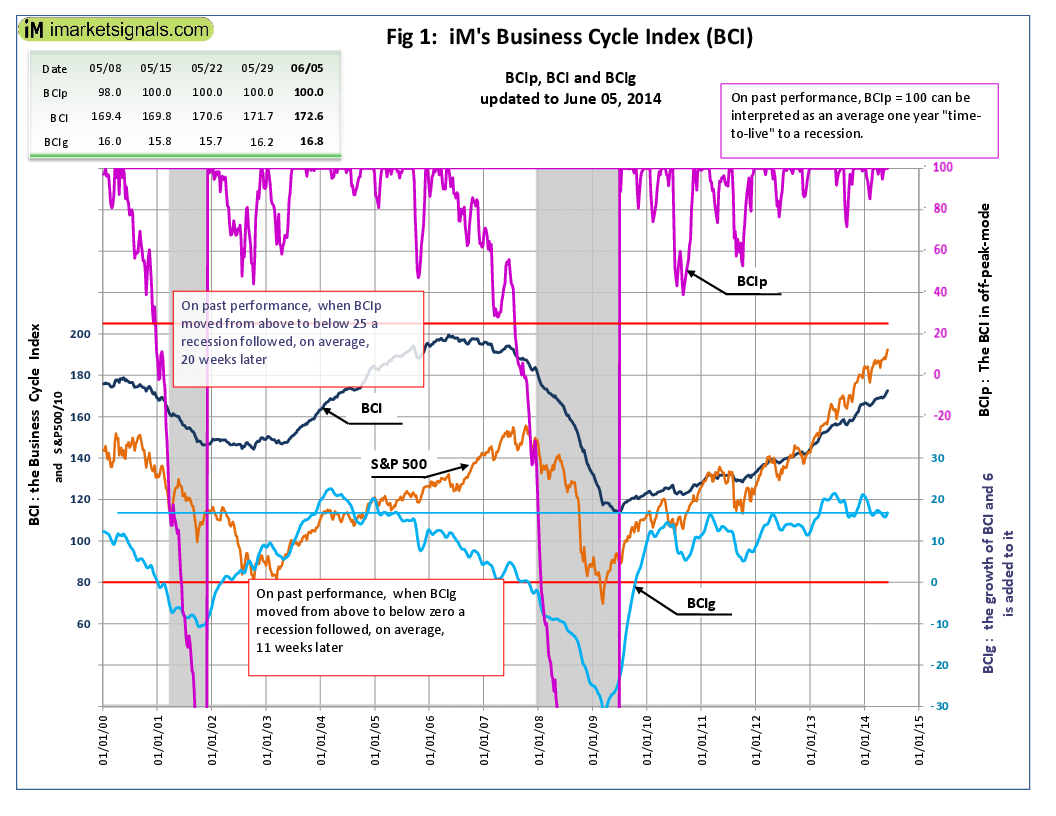

The BCI at 172.6 is up from last week’s upward revised 171.7. The BCIg, the smoothed annualized growth of BCI, at 16.8 is also up from last week’s 16.2.

The BCI at 172.6 is up from last week’s upward revised 171.7. The BCIg, the smoothed annualized growth of BCI, at 16.8 is also up from last week’s 16.2.

Read more >

Blog Archives

BCI June 5, 2014

Posted in pmp BCI

iM Update* – May 30 2014

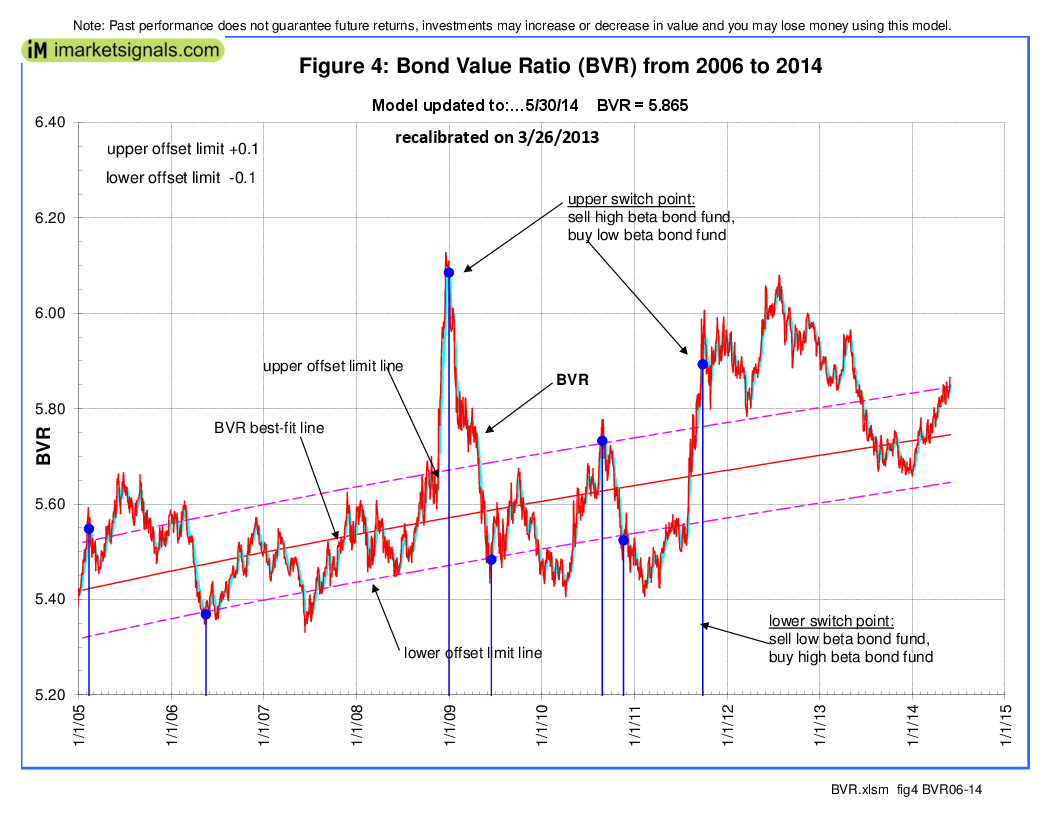

The BVR-model avoids high beta bonds (long-bonds) and also intermediate duration bonds. The Bond Value Ratio is shown in Fig 4. The BVR is higher than last week’s level. According to the model, only when BVR turns upward after having been lower than the lower offset-line should one consider long bonds again.

The BVR-model avoids high beta bonds (long-bonds) and also intermediate duration bonds. The Bond Value Ratio is shown in Fig 4. The BVR is higher than last week’s level. According to the model, only when BVR turns upward after having been lower than the lower offset-line should one consider long bonds again.

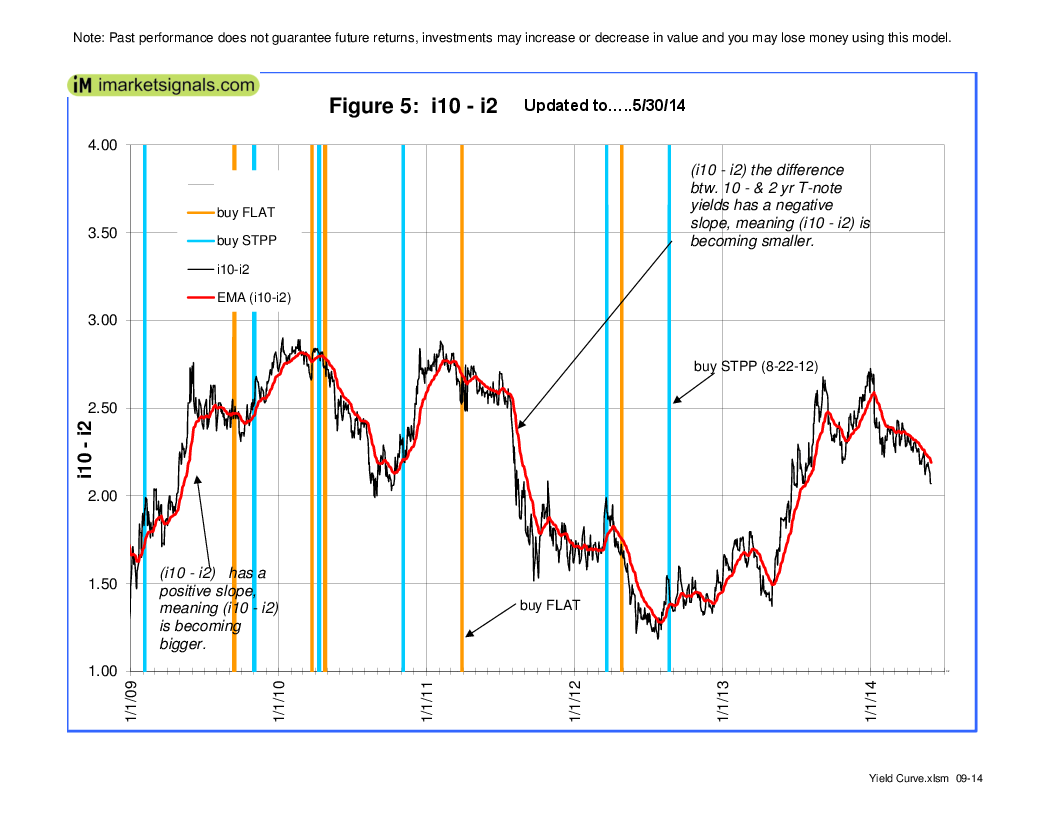

The yield curve model shows the generally steepening trend of the 10-year and 2-year Treasuries yield spread. Figure 5 charts (i10 – i2). The general trend is up, as one can see, although the yield curve has flattened recently. FLAT and STPP are ETNs. STPP profits from a steepening yield curve and FLAT increases in value when the yield curve flattens. This model confirms the direction of the BVR.

The yield curve model shows the generally steepening trend of the 10-year and 2-year Treasuries yield spread. Figure 5 charts (i10 – i2). The general trend is up, as one can see, although the yield curve has flattened recently. FLAT and STPP are ETNs. STPP profits from a steepening yield curve and FLAT increases in value when the yield curve flattens. This model confirms the direction of the BVR.

Posted in pmp paid update

BCI May 29, 2014

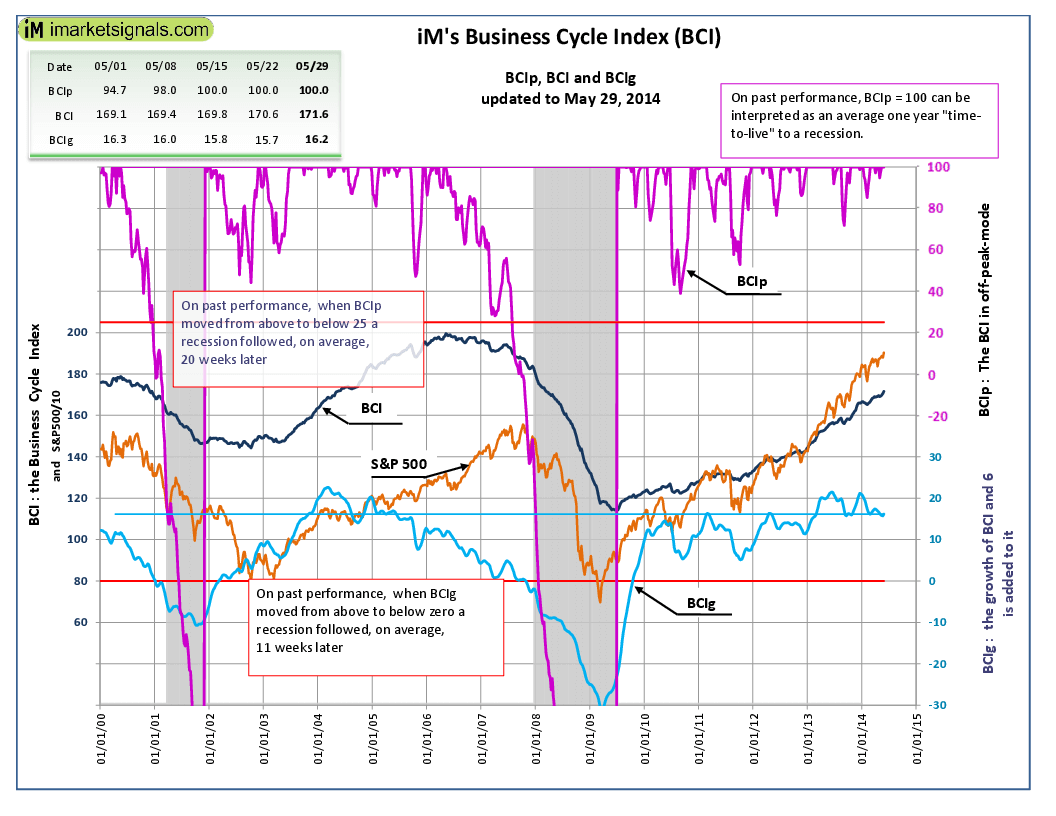

The BCI at 171.6 is up from last week’s upward revised 170.6. The BCIg, the smoothed annualized growth of BCI, at 16.2 is also up from last week’s upward revised 15.7.

The BCI at 171.6 is up from last week’s upward revised 170.6. The BCIg, the smoothed annualized growth of BCI, at 16.2 is also up from last week’s upward revised 15.7.

Read more >

Posted in pmp BCI

iM Update* – May 23, 2014

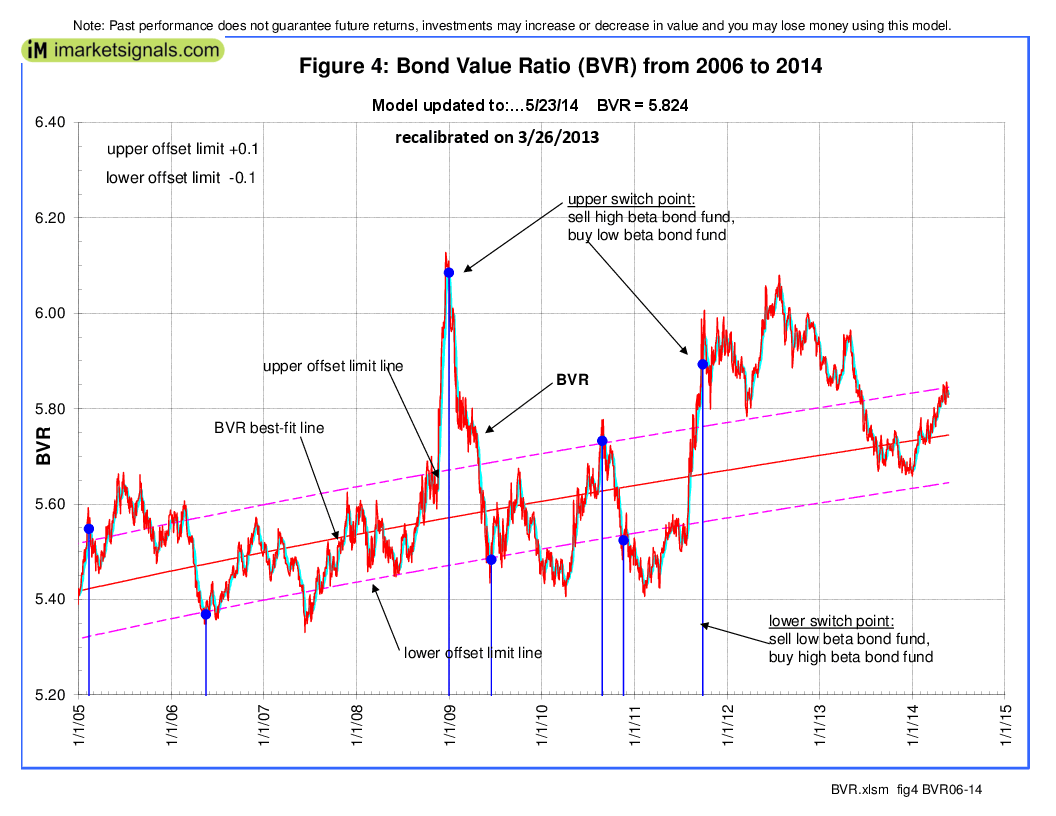

The BVR-model avoids high beta bonds (long-bonds) and also intermediate duration bonds. The Bond Value Ratio is shown in Fig 4. The BVR is a bit lower than last week’s level. According to the model, only when BVR turns upward after having been lower than the lower offset-line should one consider long bonds again.

The BVR-model avoids high beta bonds (long-bonds) and also intermediate duration bonds. The Bond Value Ratio is shown in Fig 4. The BVR is a bit lower than last week’s level. According to the model, only when BVR turns upward after having been lower than the lower offset-line should one consider long bonds again.

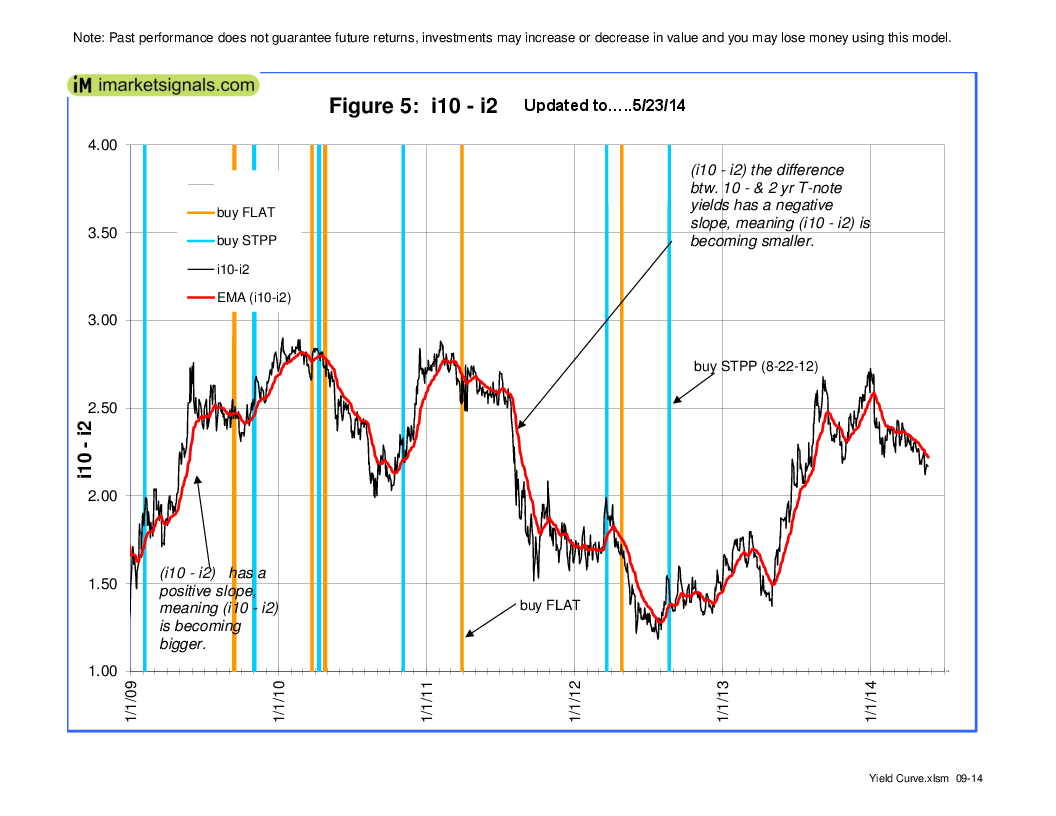

The yield curve model shows the generally steepening trend of the 10-year and 2-year Treasuries yield spread. Figure 5 charts (i10 – i2). The general trend is up, as one can see, although the yield curve has flattened recently. FLAT and STPP are ETNs. STPP profits from a steepening yield curve and FLAT increases in value when the yield curve flattens. This model confirms the direction of the BVR.

The yield curve model shows the generally steepening trend of the 10-year and 2-year Treasuries yield spread. Figure 5 charts (i10 – i2). The general trend is up, as one can see, although the yield curve has flattened recently. FLAT and STPP are ETNs. STPP profits from a steepening yield curve and FLAT increases in value when the yield curve flattens. This model confirms the direction of the BVR.

Posted in pmp paid update

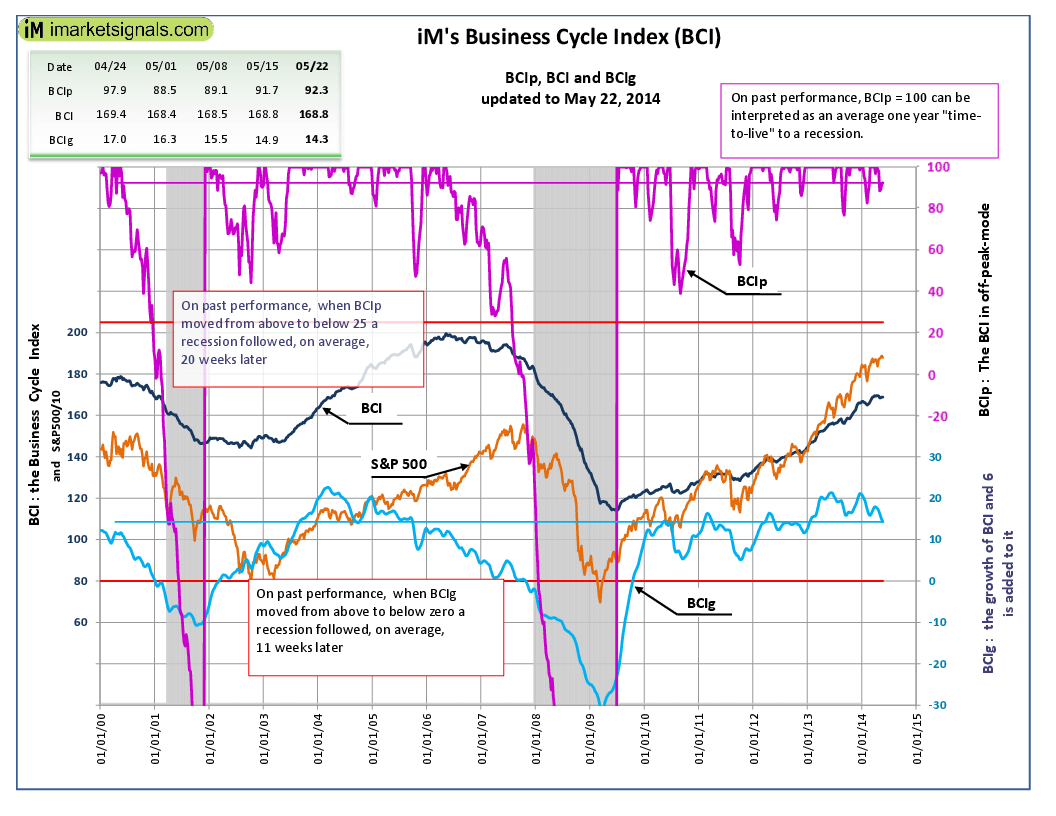

BCI May 22, 2014

The BCI is unchanged from last week’s 168.8. However, the BCIg, the smoothed annualized growth of BCI, is down at 14.3 from last week’s 14.9.

The BCI is unchanged from last week’s 168.8. However, the BCIg, the smoothed annualized growth of BCI, is down at 14.3 from last week’s 14.9.

Read more >

Posted in pmp BCI

Best(SPY-SH) and Combo3 – 5/19/2014

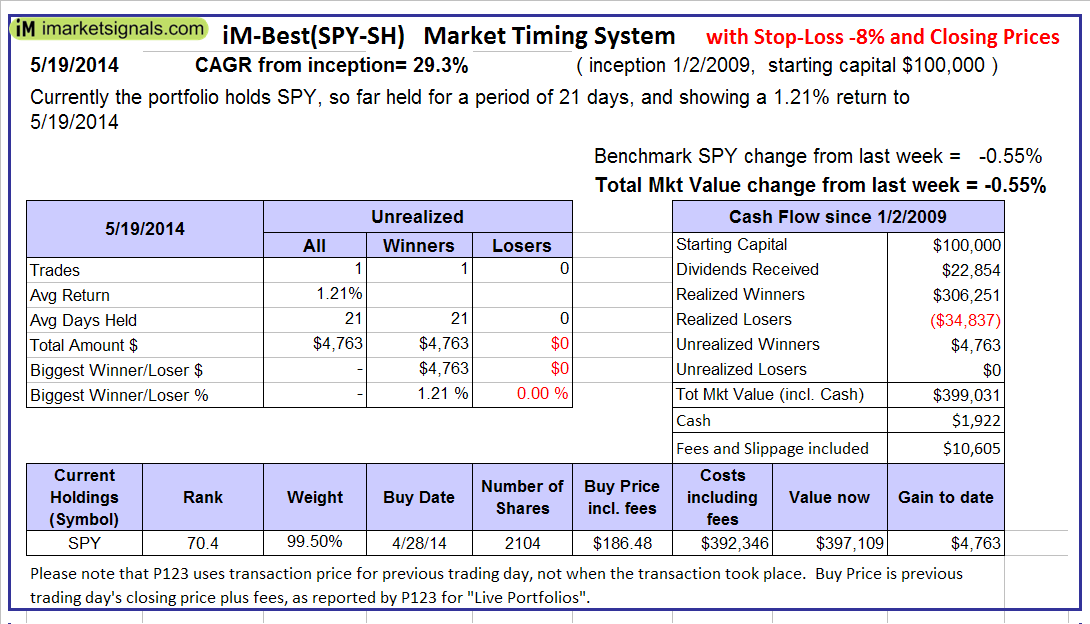

The iM-Best(SPY-SH) model currently holds SPY, so far held for a period of 21 days, and showing 1.21% return to5/19/2014

The iM-Best(SPY-SH) model currently holds SPY, so far held for a period of 21 days, and showing 1.21% return to5/19/2014

Read more >

Posted in pmp SPY-SH

With reference to Section 202(a)(11)(D) of the Investment Advisers Act:

We are Engineers and not Investment Advisers,

read more ...

By the mere act of reading this page and navigating this site you acknowledge, agree to, and abide by the

Terms of Use / Disclaimer