- The Vanguard Market Neutral Fund Investor Shares (VMNFX) aims to “neutralize”, or limit the effect of stock market movement on returns.

- We calculate 26-week rolling returns for VMNFX and for benchmark SPY (the ETF tracking the S&P500), which provide a measure of over- or under performance of VMNFX relative to SPY.

- Predictive information comes from the relationship between the fund and the benchmark rolling returns. If VMNFX performs better than the stock market then one should be out of the market.

- Conversely, if VMNFX under performs SPY then it should be relatively safe to be invested in stocks.

- Our analysis generated a sell signal for the stock market on Nov-2-2015.

The VMNFX Market Timing System

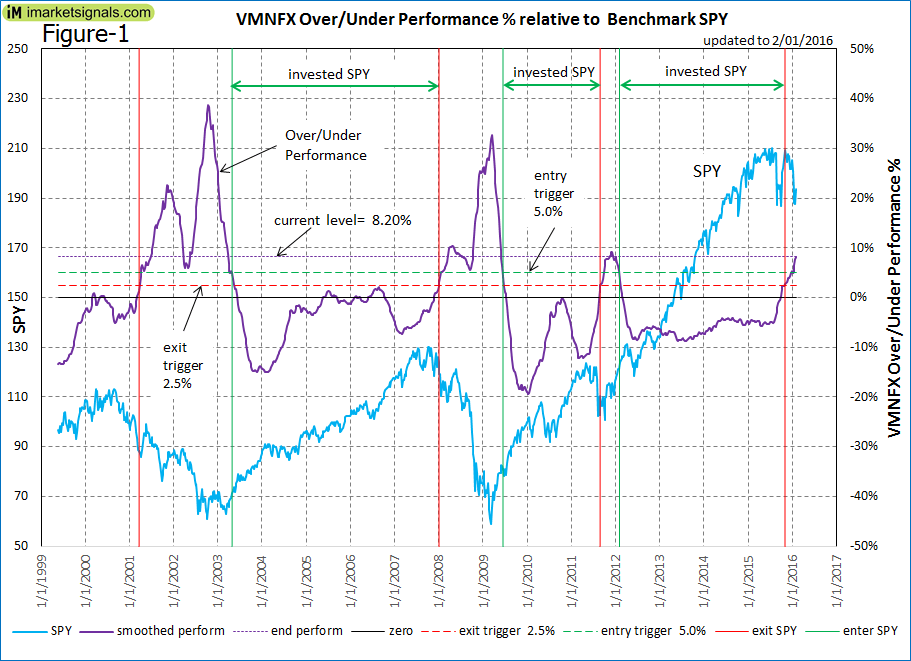

Figure-1 shows the smoothed weekly relative performance from 1999 to 2016. The exit- and entry triggers for the stock market were set at +2.5% and +5.0% relative performance, respectively. These levels were chosen to provide the least number of signals and early exit- and entry dates.

Thus, when relative performance becomes greater than 2.5% a sell signal for the stock market arises. Conversely, when relative performance becomes less than 5.0% a market entry signal is generated.

The historic out-of-market periods signaled by this model were:

03/26/2001 – 05/05/2003

01/07/2008 – 06/15/2009

08/29/2011 – 02/06/2012 (false positive)

11/02/2015 – ???

Return Comparisons

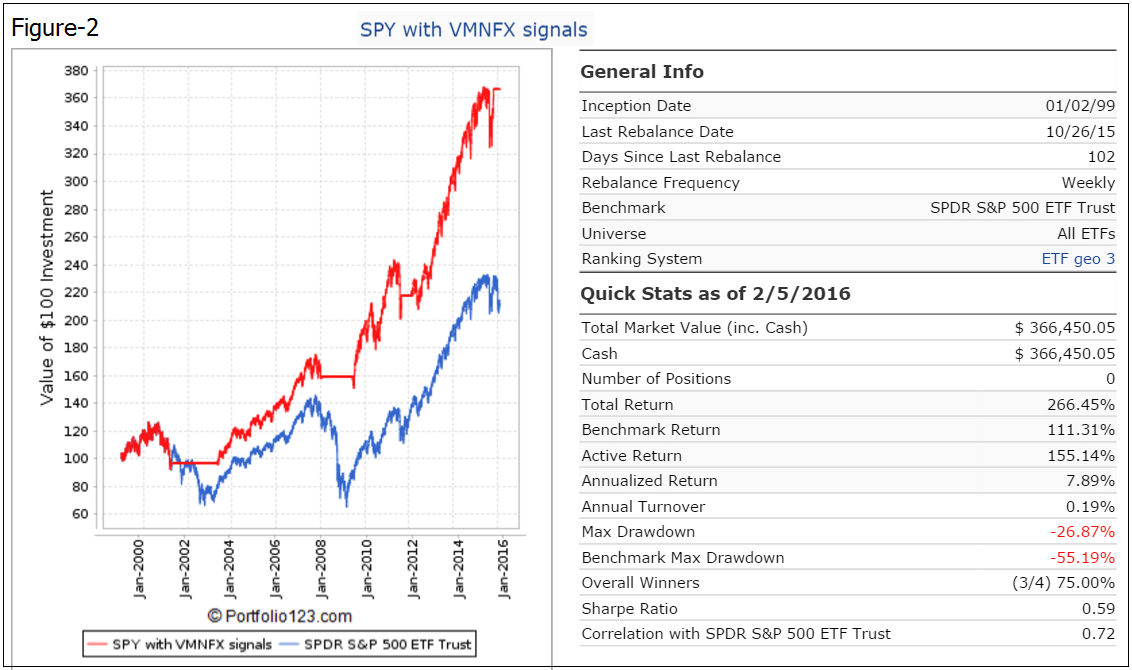

The total buy-and-hold return for SPY from the beginning of Jan-1999 to beginning of Feb-2016 was 111.3%, which is an annualized return of 4.47%, and the maximum drawdown was -55.2%.

An investment in SPY with the out-of-market periods in Cash would have provided from the beginning of Jan-1999 to beginning of Feb-2016 a total return of 266.5%, which is an annualized return of 7.89%, and the maximum drawdown would have been -26.9%.

Figure 2 shows graphically the performance of SPY (blue graph) and of SPY with VMNFX signals (red graph), calculated on the web-based simulation platform Portfolio 123.

Conclusion

It appears that the performance of the Vanguard Market Neutral Fund VMNFX relative to SPY is a good indicator for major stock market movements. The last exit signal occurred on Nov-2-2015. The most recent relative performance is at 8.15%, which is near the Dec-2011 peak level of 9.17%. Should the relative performance continue much above the current level, then further market declines are possible.

This technical timing model is simple and can be reproduced without much difficulty. However, those not wanting to replicate it can visit our website imarketsignals.com where it will be updated weekly.

Another of your many creative and well-thought-out approaches. How does this model correlate with some of your standards, such as COMBO3 and SPY/IEF? In fact, it would be interesting to see an article at some point on which of your various newer systems have relatively low correlations with COMBO3, SPY/IEF, and one another. Diversification in the models is as important to me as in stocks and bonds themselves.

On this model, I am wondering about the possible lost opportunity cost if it triggers an exit crossing 2.5 but falls back before reaching 5 and so does not trigger a reentry. This came close to happening in the sample in 2005, 2006, and the slight false positive in 2011. Slightly different values at those points could have left the model missing large chunks of bull market. Would it be better to treat the area between 2.5 and 5 as 50/50 in the market, above 5 out of the market, and below 2.5 in the market?

Thanks for the great work.

This is a macro model with very few signals. Combo3 and SPY-IEF are combo models with a lot of signals, that is why their returns are so much higher.

“Would it be better to treat the area between 2.5 and 5 as 50/50 in the market, above 5 out of the market, and below 2.5 in the market?”

This is a good question that will need some more analysis to answer. We will get back to this later. Thanks.

You’ve certainly been busy turning out a lot of new interesting models in the last few weeks. I’m hoping at some point you can get back to the question above, as I think this model could be useful for diversification in conjunction with some of your other models. Thanks.

Hello Georg, I like the theory but I’m confused about how to replicate the calculations. During the last 26 weeks, SPY went from 210.50 to 187.95 (-10.71%), and VMNFX went from 11.66 to 12.30 (+5.49%). The current difference between their 26-week performances is ~16%. The chart above shows the current level is 8.2%. I’m obviously misunderstanding something or missing a few steps.

The description says that we are using a smoothed weekly relative performance. That means that the data is smoothed with exponential moving averages. The relative performance percentage is calculated as (26-week return of VMNFX / 26-week return of SPY)- 1.00.

Got it, thank you!

In regards to 2011-12, don’t forget we had QE that can distort any calculations with whipsaws. Similar to today, you need to make your own decision then.