Market Signals Summary:

The 3-mo Hi-Lo Index is out of the market since 3/5/2020 and the MAC US and the MAC AU also switched out begining this week. The bond market model avoids high beta (long) bonds, and the yield curve is steepening and signaled a buy STPP. The Gold Coppock remains in gold but the iM-Gold Timer is in cash, also the silver model is in cash.

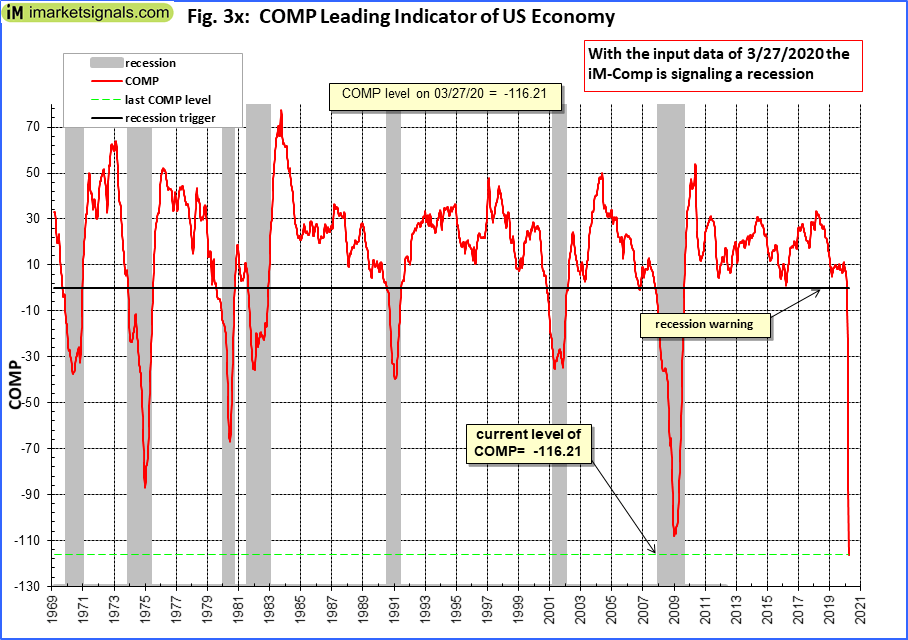

The iM-COMP leading indicator of the US economy signals a recession

The iM-GT Timer, based on Google Search Trends volume switched out of the markets on 3/5/2020.

Stock-markets:

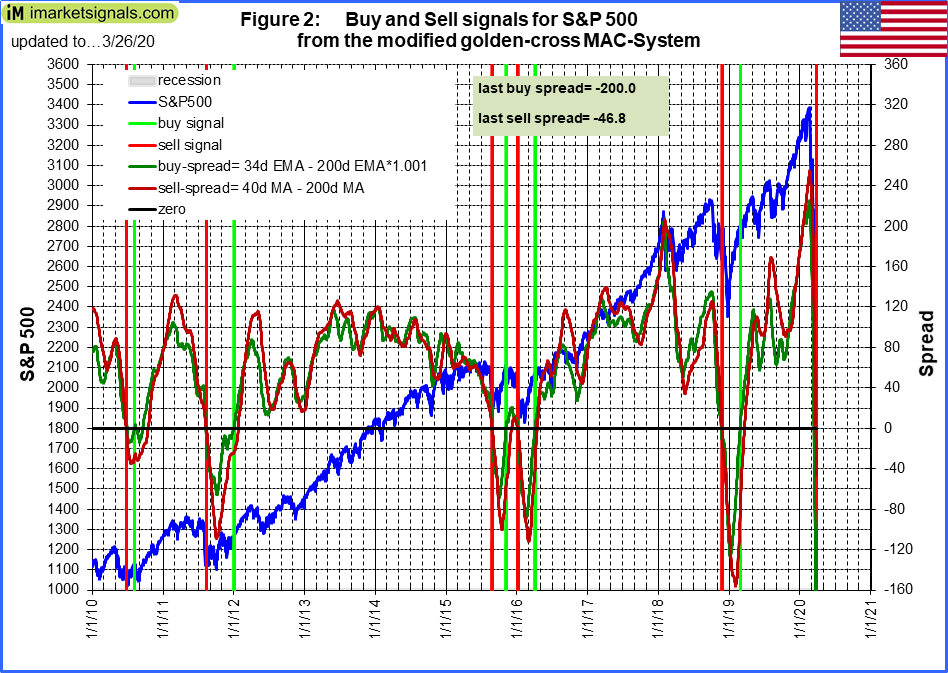

The MAC-US model switched out of the markets. The sell-spread (red line) is below last week’s value.

The MAC-US model switched out of the markets. The sell-spread (red line) is below last week’s value.

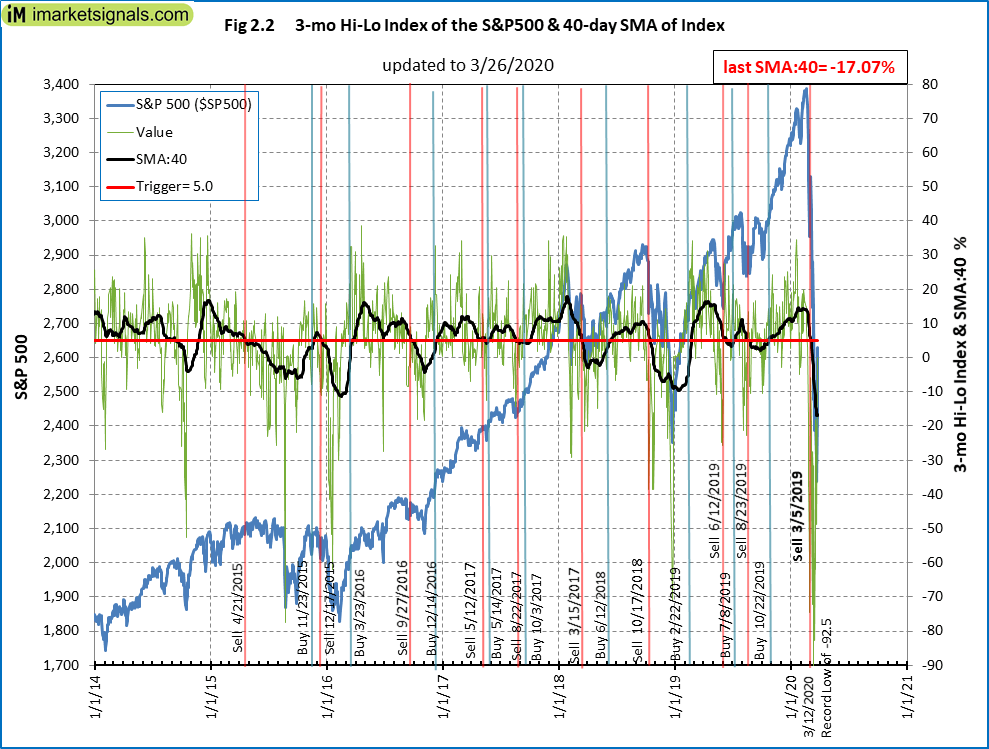

The 3-mo Hi-Lo Index Index of the S&P500 at -17.07% is below last week’s -14.40%, and is out of the stock market since 3/5/2020.

The 3-mo Hi-Lo Index Index of the S&P500 at -17.07% is below last week’s -14.40%, and is out of the stock market since 3/5/2020.

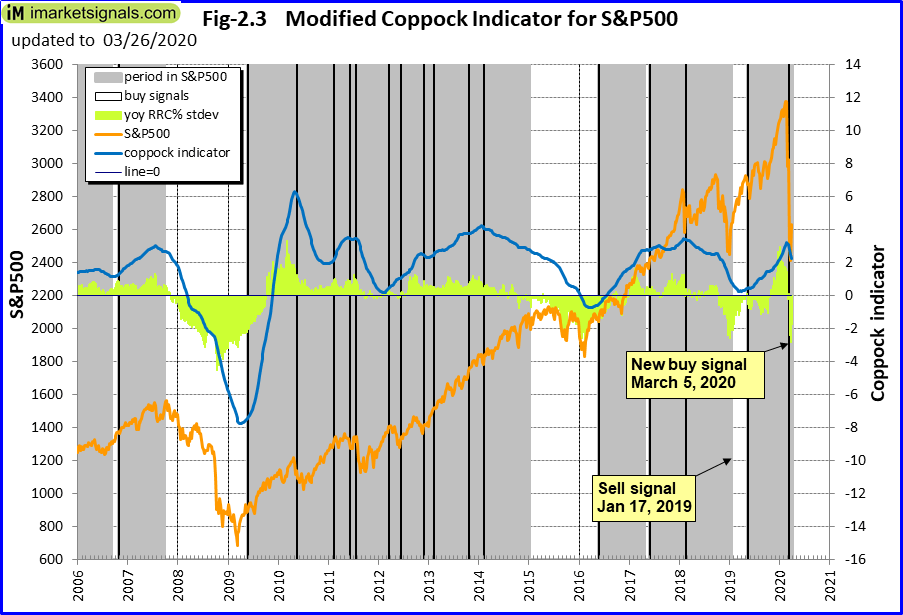

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

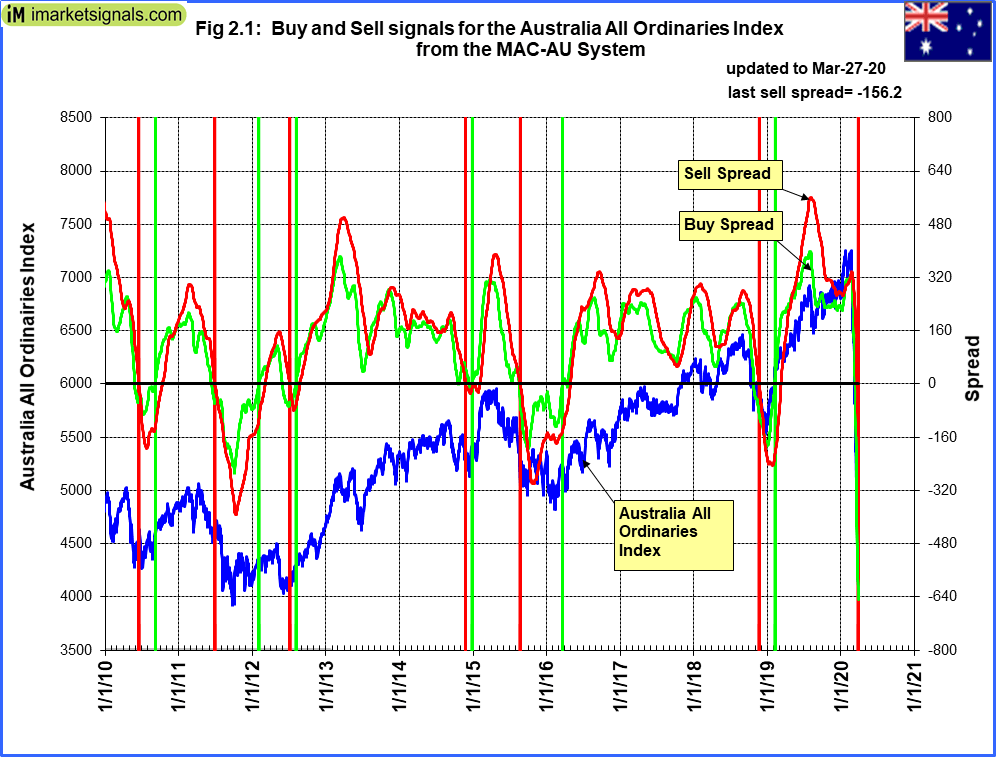

The MAC-AU model switch out of the markets. The sell-spread (red line) is below last week’s value.

The MAC-AU model switch out of the markets. The sell-spread (red line) is below last week’s value.

This model and its application is described in MAC-Australia: A Moving Average Crossover System for Superannuation Asset Allocations.

Recession:

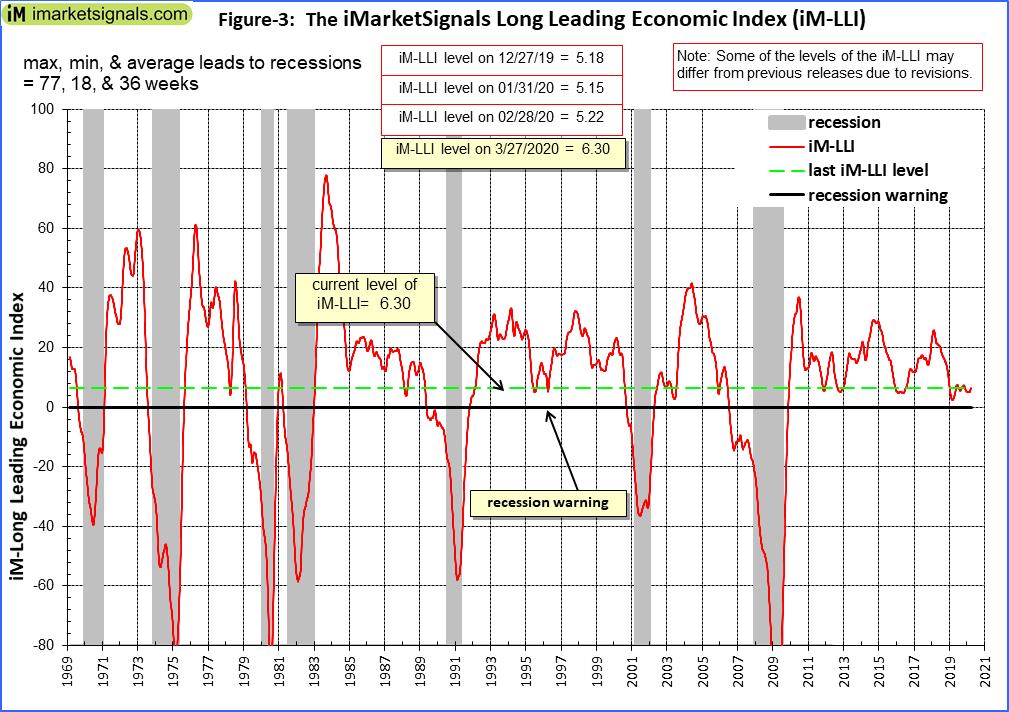

The current level of iM-LLI is at plus 5.57 and is above last week’s 5.43, hence this indicator signals that a recession is unlikely to begin during the next 8 months. The effect of the COVID-19 pandemic is not reflected in this series.

The current level of iM-LLI is at plus 5.57 and is above last week’s 5.43, hence this indicator signals that a recession is unlikely to begin during the next 8 months. The effect of the COVID-19 pandemic is not reflected in this series.

Although we discontinied COMP, we updated it weekly and with the input data of 3/27/2020 signals a recession. This model uses following three components: (i) ECRI’s WLIW, (ii) Aruoba-Diebold-Scotti Business Conditions Index (ADS), and (iii) The Conference Board Leading Economic Index® (LEI) for the U.S Mainly the ADS drove the COMP downwards.

Although we discontinied COMP, we updated it weekly and with the input data of 3/27/2020 signals a recession. This model uses following three components: (i) ECRI’s WLIW, (ii) Aruoba-Diebold-Scotti Business Conditions Index (ADS), and (iii) The Conference Board Leading Economic Index® (LEI) for the U.S Mainly the ADS drove the COMP downwards.

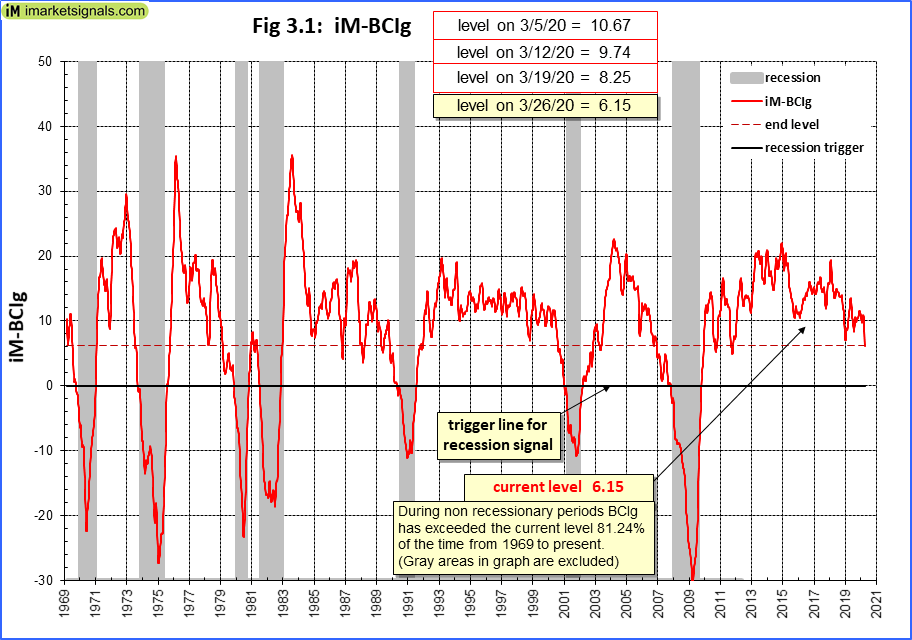

Figure 3.1 shows the recession indicator iM-BCIg below last week’s level. The effect of the COVID-19 pandemic is not reflected in this series.

Figure 3.1 shows the recession indicator iM-BCIg below last week’s level. The effect of the COVID-19 pandemic is not reflected in this series.

Please also refer to the BCI page

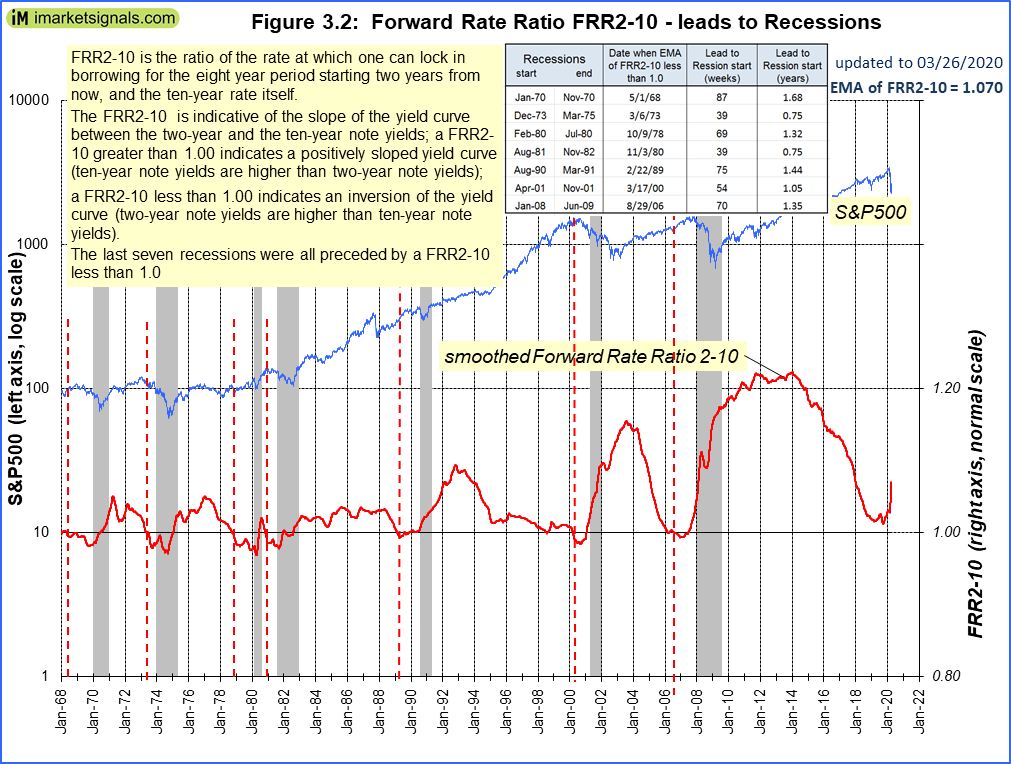

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is above last week’s level and is not signaling a recession.

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is above last week’s level and is not signaling a recession.

A description of this indicator can be found here.

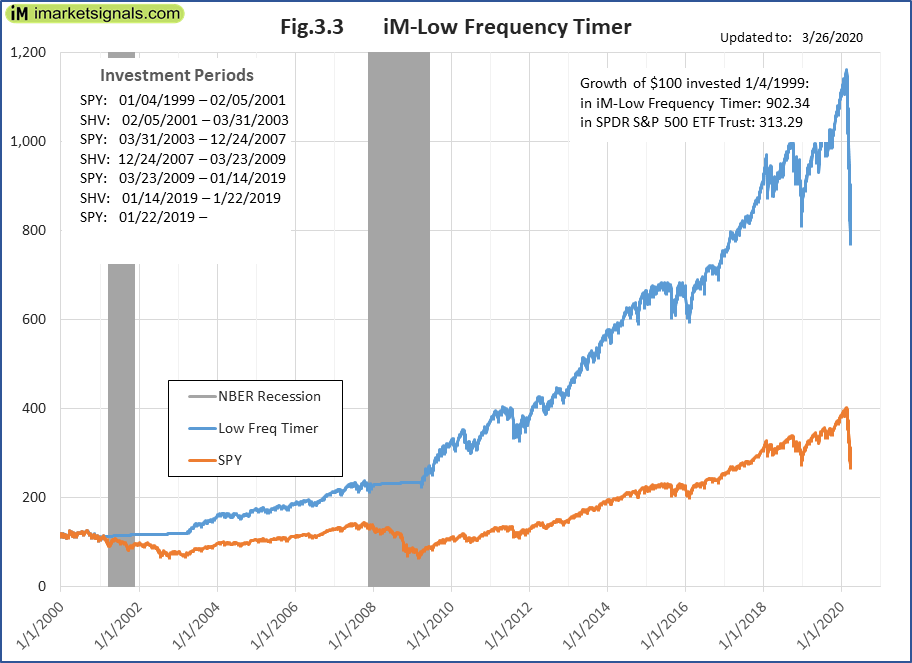

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

A description of this indicator can be found here.

Leave a Reply

You must be logged in to post a comment.