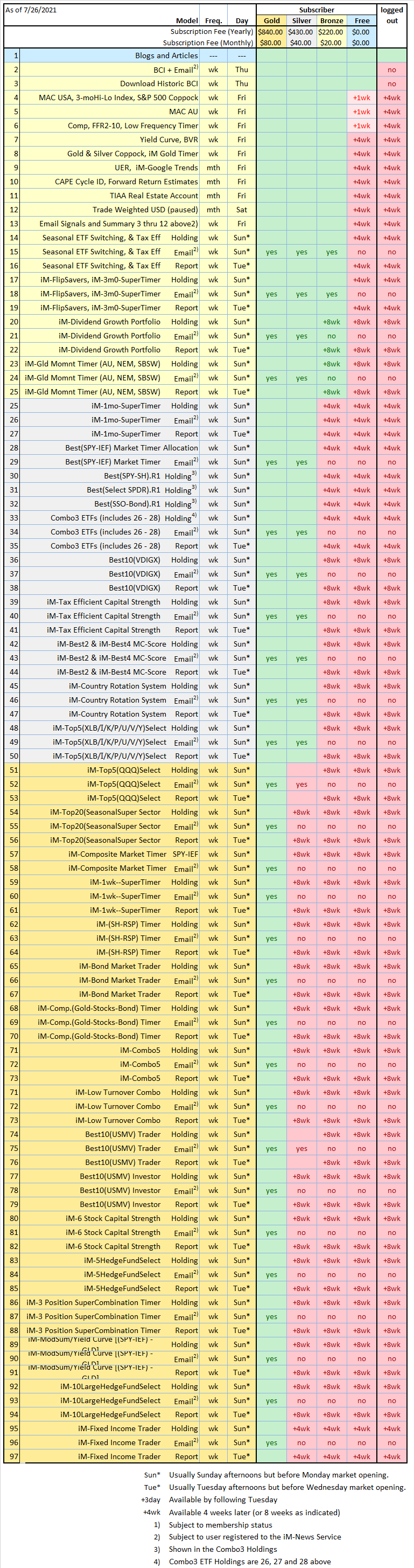

How is the Bond Value Ratio calculated?The Bond Value Ratio is my proprietary indicator for the trend of US treasury bond yields, and is described in

Seeking Beta in the Bond Market: A Math-driven Investment Strategy for Higher Returns.

The “Bond Value Ratio” (BVR), is based on the daily yields-to-maturity of the 30-year Treasury bond (i30) and the 10-year note (i10). Bond values derive from the daily yields, and the relationship between those bond values is captured by the BVR, which is an indicator of up or down bond markets. BVR increases if the value change of the 30-year bond exceeds the value change of the 10-year note (an up bond market), and vice versa.

BVR will increase under the following conditions:

- i30 and i10 decreases by the same amount. This is a parallel shift of the yield curve but the long bond will gain more than the 10 year note.

- i30 and i10 decrease both by different amounts, but the long bond gains more than the 10 year note.

- i30 is constant and i10 increases. The value of the long bond will not change but the 10 year note will decrease in value.

- i30 and i10 both increase but i10 increases much more than i30. Although the value of the 30 year bond becomes less, the 10 year note looses more value than the 30 year bond.

The upper switch points are generated when BVR is above the upper offset line and turns downwards. At upper switch points the model suggests to sell high (long) bonds and switch into cash or low beta (short) bonds. And vice versa for the lower switch points.

How is the level of COMP calculated?The three component indices listed in appendix A of

The Use of Recession Indicators in Stock Market Timing are used to produce the COMP. They are normalized and proprietary weightings are applied to them, optimized to produce the highest score from my recession indicator evaluation system described in

Evaluating Popular Recession Indicators.

Can the MAC-system be applied to markets outside the US?No, the MAC-system only applies to the S&P500 stock market index.

What would have happened if the MAC-system’s sell spread after a buy signal in mid-2010 never crossed above the zero-line?Then one would have been constantly invested because one would not have had a sell signal in August 2011.

How does one handle periods when both a buy signal and a sell signal from the MAC-system are in place; which signal takes precedence and why? (I had been thinking that the buy and sell signals were independent, and they each remained in force as long as they continued to exceed their respective spreads. Since they have different time lags, there are many occasions where they overlap.)

There is no such condition as a period when both a buy signal and a sell signal are in place, because the signals can only occur on one particular day. A sell signal can only occur when the model is in the market, and a buy signal can only occur when the model is out of the market.

What happens when one is out of the market due to a previous sell signal from the MAC-system, then a buy signal is given, but it turns out that the buy signal was triggered by a temporary pop in the stock market as opposed to a sustained trend change? If the market then proceeds to decline in a long trend, wouldn’t that cause the model to remain in the market?Yes, the MAC model would remain in the market.

I know the IBH-model generates three types of buy/sell signals but I am unsure as to how to use them. Are they intended for scaling in and out of the market? For example, if a basic buy is generated do you invest one third of the portfolio followed by remaining thirds after each of the A and B signals?The model does not have a basic buy signal. There are types A, B, and C buy signals. The model assumes that one would buy immediately when the first buy signal occurs. Subsequent buy signals which may occur before a sell signals are ignored.

I just read today that the ECRI is constantly revising their past weekly data. Have you found this to be a problem? One can only go with the data as it is presented, and if one were back-testing, how would one know they revised the data later, which could seriously alter one’s signals?I was aware that ECRI revises their data periodically but I have not seen them doing it before for such a long period. The latest revision is from Jan-2011 to Sep-2011. I re-calculated my spreadsheet with the revised data (back-testing) and the Sell-basic signal appears now 2 weeks later on May 25, 2011. So there is a marginal difference here which does not rally affect the IBH-model.

Next questionplace holder for answer