Market Signals Summary:

All iM US market macro models are in the stock market as is the australian MAC-AU. The recession indicators iM-LLI and iM-BCIg do not signal a recession. The bond market model avoids high beta (long) bonds, and the yield curve is flattening and a buy FLAT was generated 2/21/2020 and the BVR reached a new record high on 2/27/2020. The Gold Coppock and iM-Gold Timer remains invested in gold, however the silver model is in cash.

Stock-markets:

The MAC-US model switched into the markets on 2/26/2019. The sell-spread (red line) is below last week’s value and needs to move below zero to generate a sell signal.

The MAC-US model switched into the markets on 2/26/2019. The sell-spread (red line) is below last week’s value and needs to move below zero to generate a sell signal.

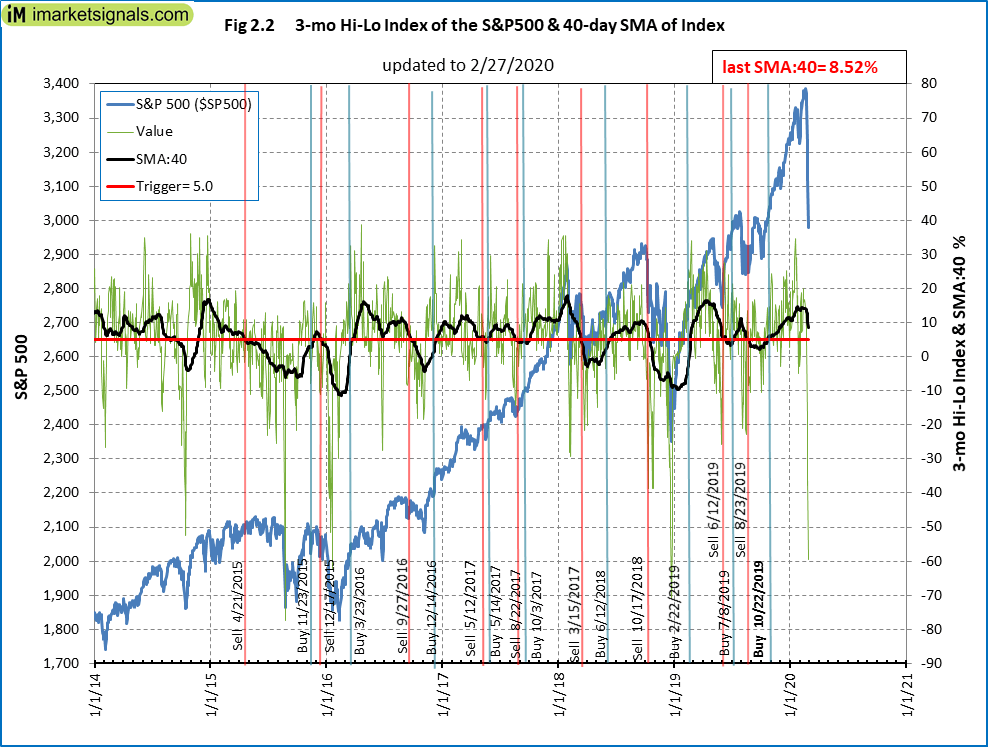

The 3-mo Hi-Lo Index Index of the S&P500 at 8.52% is below last week’s level 0f 13.69%, and is invested in the stock market since 10/22/2019.

The 3-mo Hi-Lo Index Index of the S&P500 at 8.52% is below last week’s level 0f 13.69%, and is invested in the stock market since 10/22/2019.

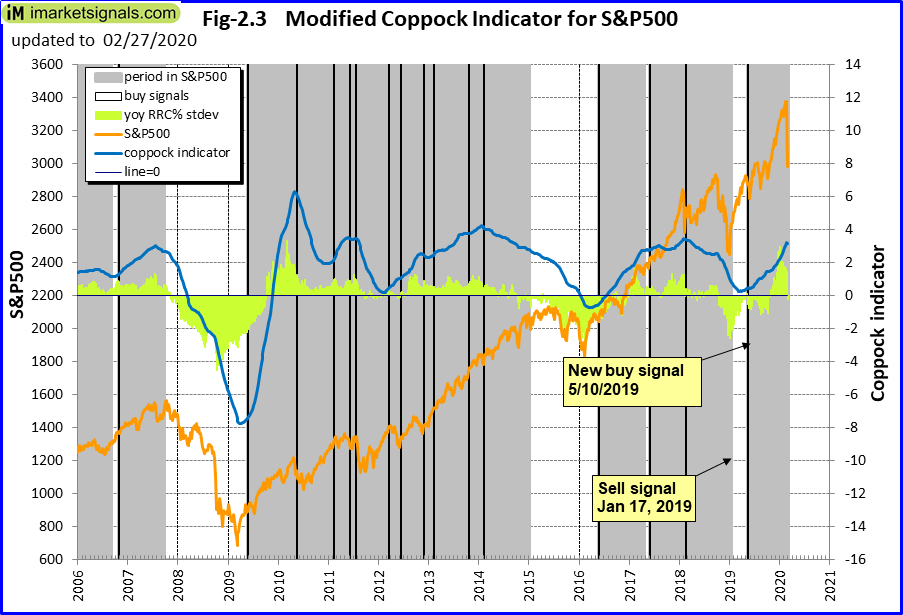

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

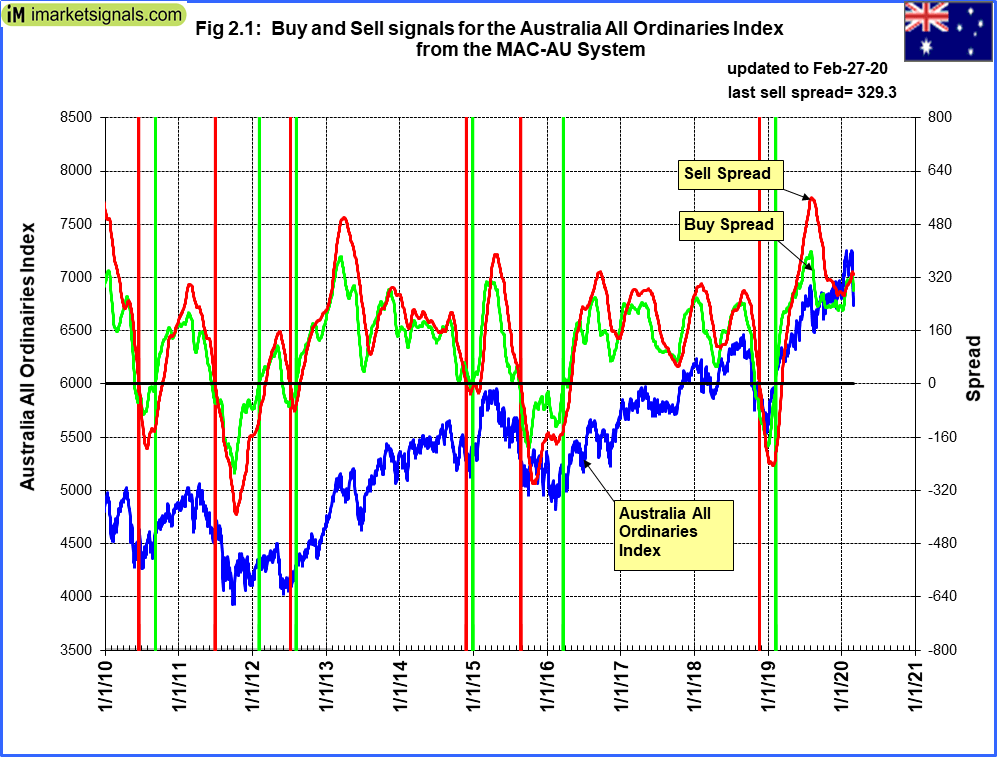

The MAC-AU model is invested in the markets. The sell-spread (red line) is near last week’s value and needs to move below zero to generate a sell signal.

The MAC-AU model is invested in the markets. The sell-spread (red line) is near last week’s value and needs to move below zero to generate a sell signal.

This model and its application is described in MAC-Australia: A Moving Average Crossover System for Superannuation Asset Allocations.

Recession:

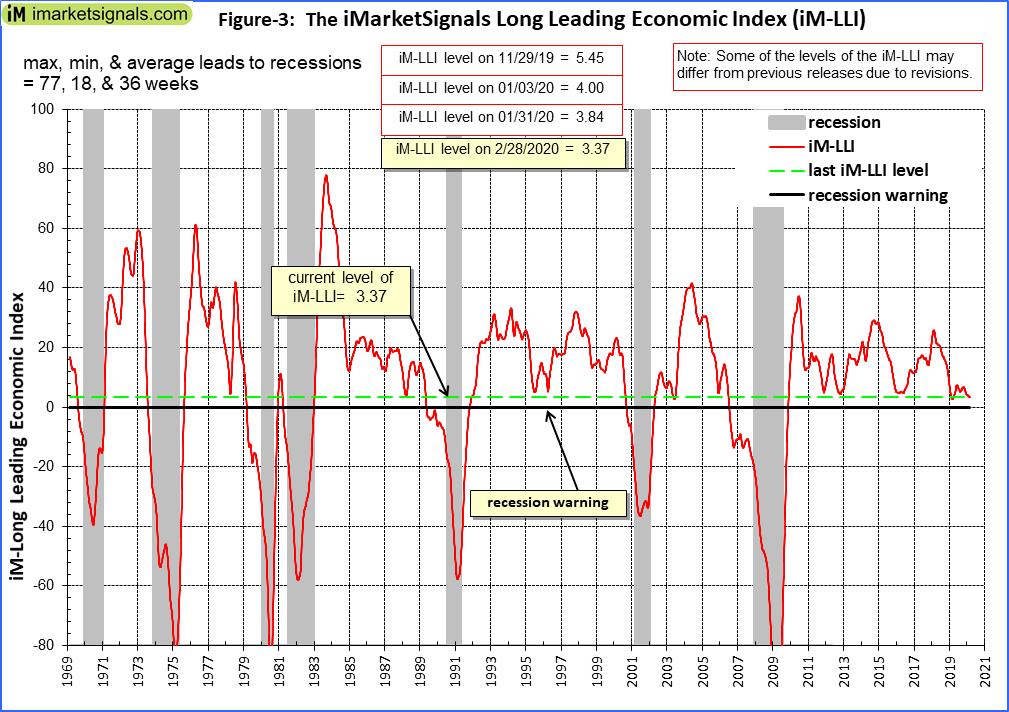

The current level of iM-LLI is plus 3.37 and is below last week’s 3.47, hence this indicator signals that a recession is unlikely to begin during the next 8 months.

The current level of iM-LLI is plus 3.37 and is below last week’s 3.47, hence this indicator signals that a recession is unlikely to begin during the next 8 months.

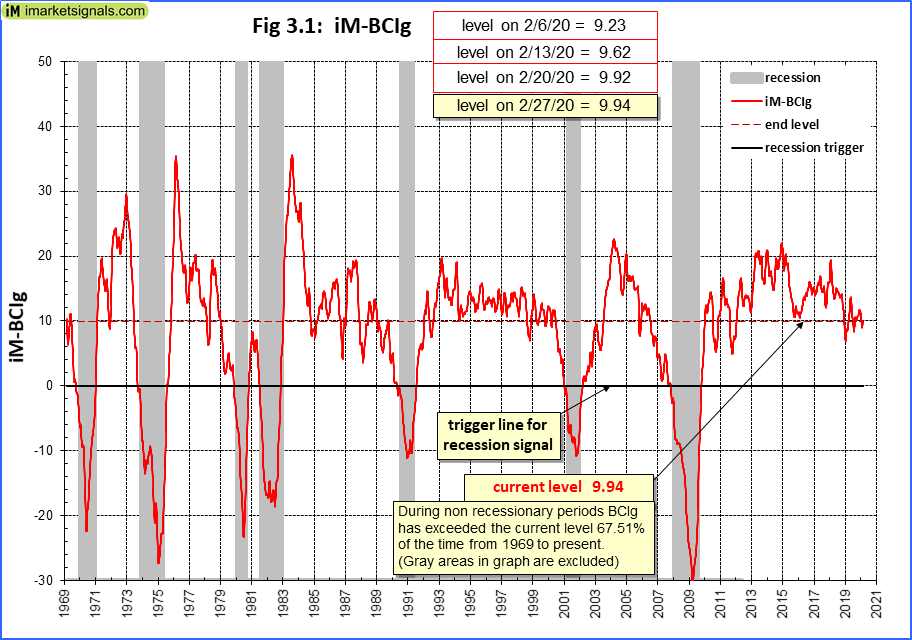

Figure 3.1 shows the recession indicator iM-BCIg at last week’s level. An imminent recession is not signaled .

Figure 3.1 shows the recession indicator iM-BCIg at last week’s level. An imminent recession is not signaled .

Please also refer to the BCI page

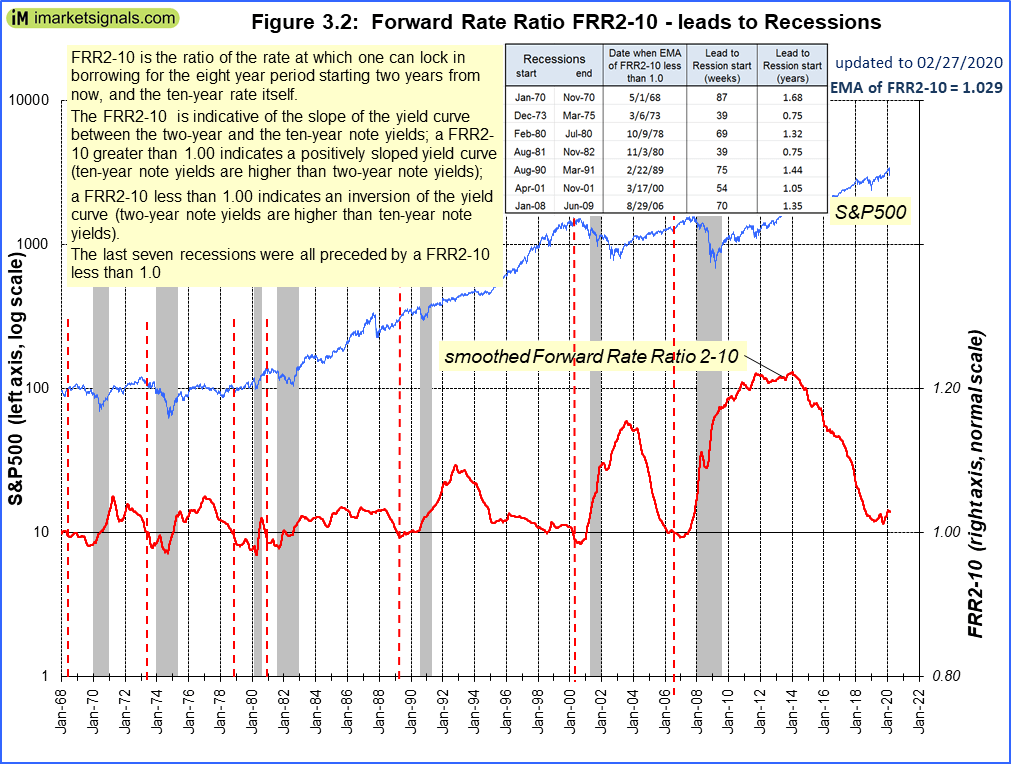

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is below last week’s level and is not signaling a recession.

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is below last week’s level and is not signaling a recession.

A description of this indicator can be found here.

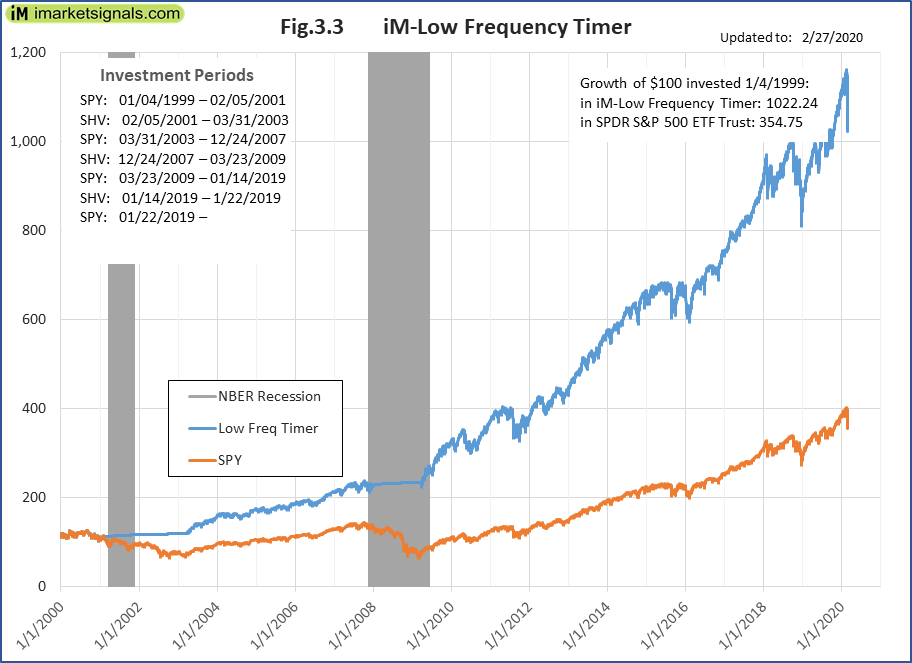

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

A description of this indicator can be found here.

Leave a Reply

You must be logged in to post a comment.