Market Signals Summary:

The MAC-US model, “3-mo Hi-Lo Index of the S&P500”, iM-Low Frequency Timer, and the S&P500 Coppock are invested in the markets. The MAC-AU is also invested in the markets. The recession indicators COMP and iM-BCIg do not signal a recession. The bond market model avoids high beta (long) bonds, and the yield curve has flattened significantly generating a buy FLAT signal. The gold Coppock remains invested in gold, however the silver model is in cash. The iM-Gold Timer is in cash.The monthly iM-GT-Timer, which is based on Google trends, is invested in the markets since July 1, 2019.

Stock-markets:

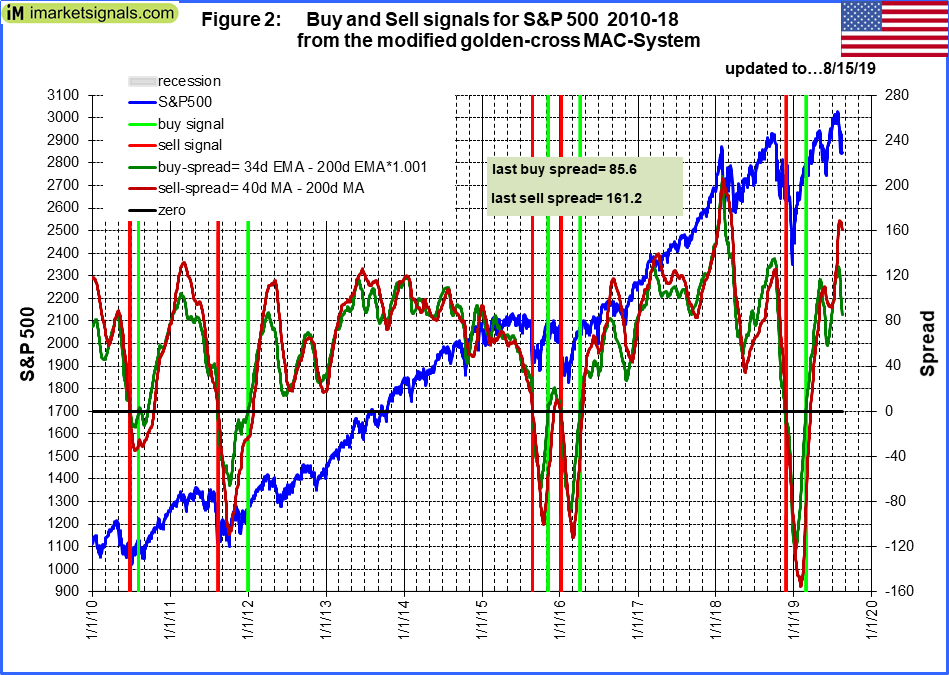

The MAC-US model switched into the markets on 2/26/2019. The sell-spread (red line) is below last week’s value needs to move below zero to generate a sell signal.

The MAC-US model switched into the markets on 2/26/2019. The sell-spread (red line) is below last week’s value needs to move below zero to generate a sell signal.

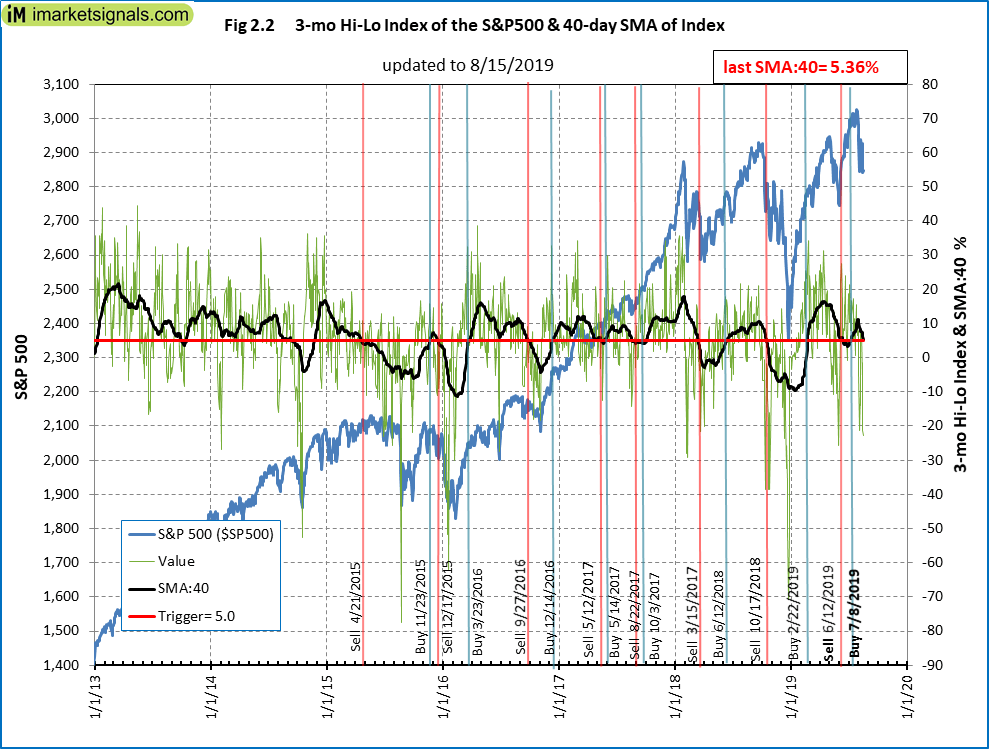

The 3-mo Hi-Lo Index Index of the S&P500 is below last week’s level at 5.36% (last week 7.77%), and is invested in the market since 7/8/2019. Simulations show that this indicator is likely to trigger a sell coming week and if the markets recovers the Hi-Lo out-of-market period will be short-lived.

The 3-mo Hi-Lo Index Index of the S&P500 is below last week’s level at 5.36% (last week 7.77%), and is invested in the market since 7/8/2019. Simulations show that this indicator is likely to trigger a sell coming week and if the markets recovers the Hi-Lo out-of-market period will be short-lived.

Update 8/18/2019 after Friday’s market close the 2-mo Hi-Lo Index dropped further to 4.91% triggering the sell signal.

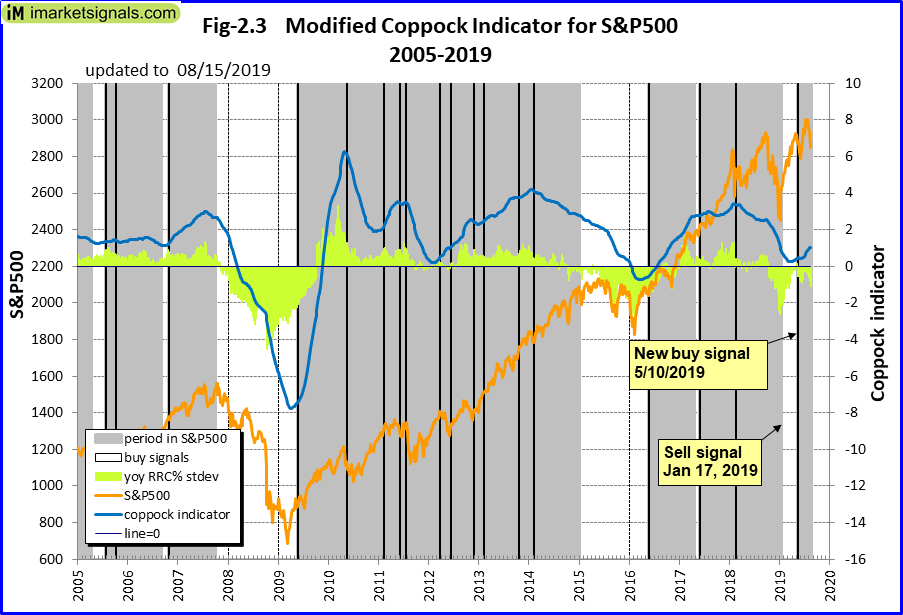

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

The Coppock indicator for the S&P500 entered the market on 5/9/2019 and is invested. This indicator is described here.

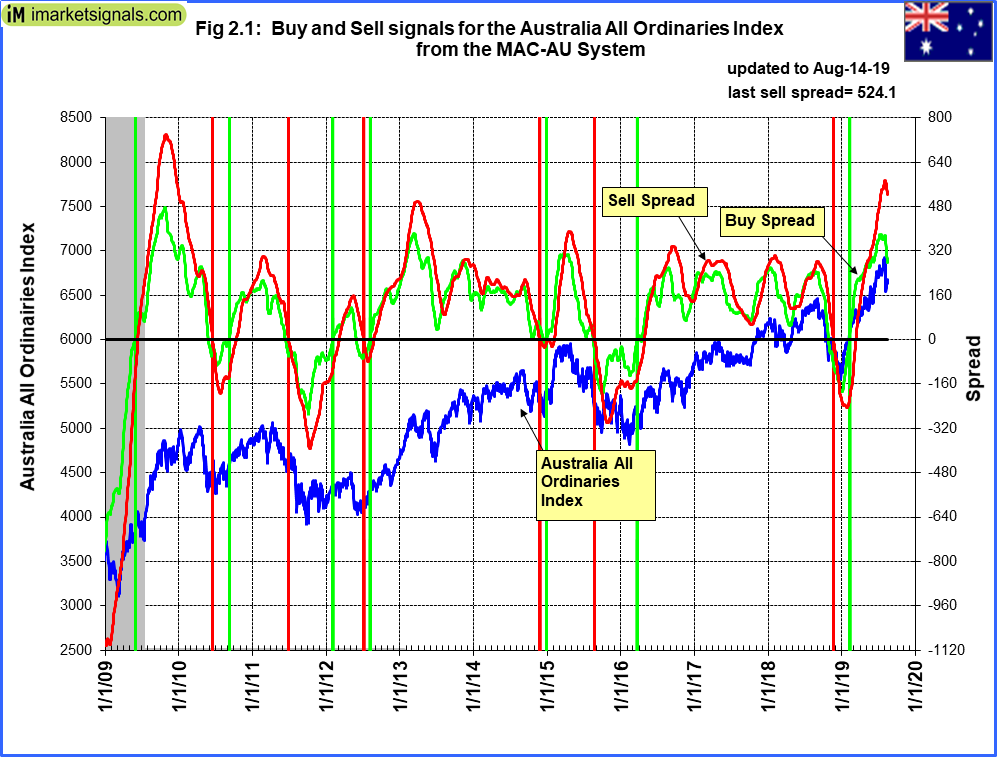

The MAC-AU model is invested in the markets after signaling a a buy on February 7, 2019. The sell-spread (red line) below last week’s value needs to move below zero to generate a sell signal.

The MAC-AU model is invested in the markets after signaling a a buy on February 7, 2019. The sell-spread (red line) below last week’s value needs to move below zero to generate a sell signal.

This model and its application is described in MAC-Australia: A Moving Average Crossover System for Superannuation Asset Allocations.

Recession:

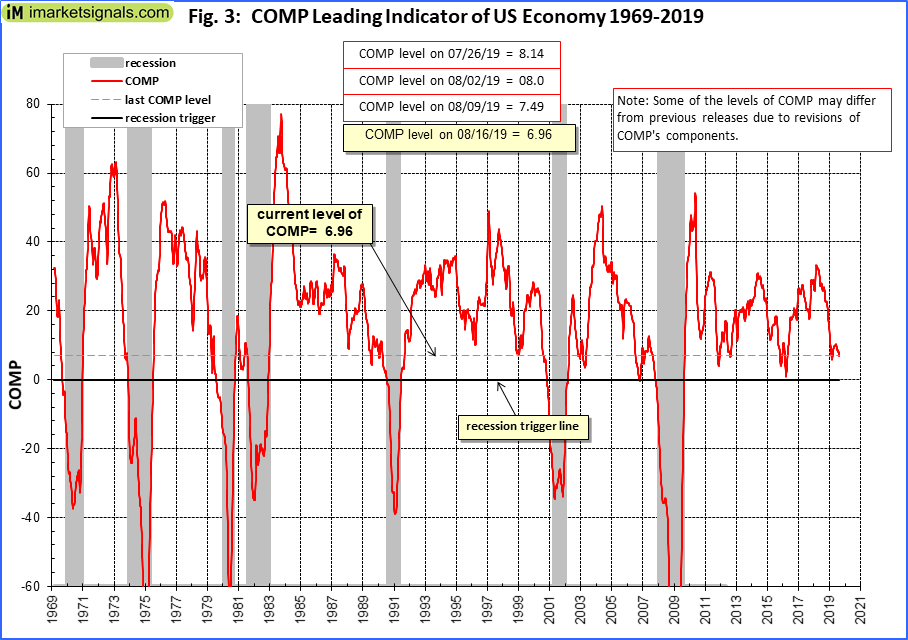

Figure 3 shows the COMP below last week’s downward revised level. No recession is indicated. COMP can be used for stock market exit timing as discussed in this article The Use of Recession Indicators in Stock Market Timing.

Figure 3 shows the COMP below last week’s downward revised level. No recession is indicated. COMP can be used for stock market exit timing as discussed in this article The Use of Recession Indicators in Stock Market Timing.

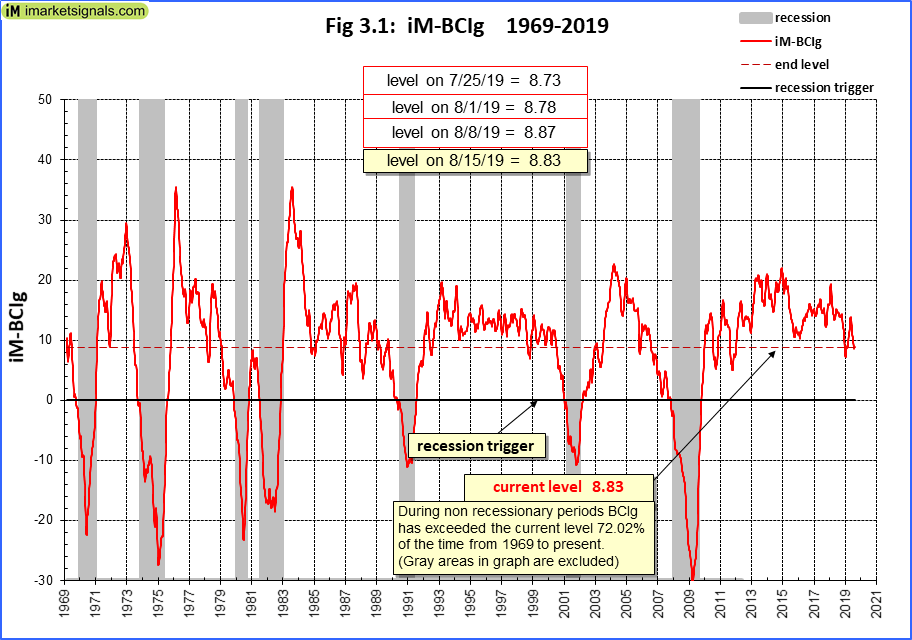

Figure 3.1 shows the recession indicator iM-BCIgbelow last week’s level. An imminent recession is not signaled .

Figure 3.1 shows the recession indicator iM-BCIgbelow last week’s level. An imminent recession is not signaled .

Please also refer to the BCI page

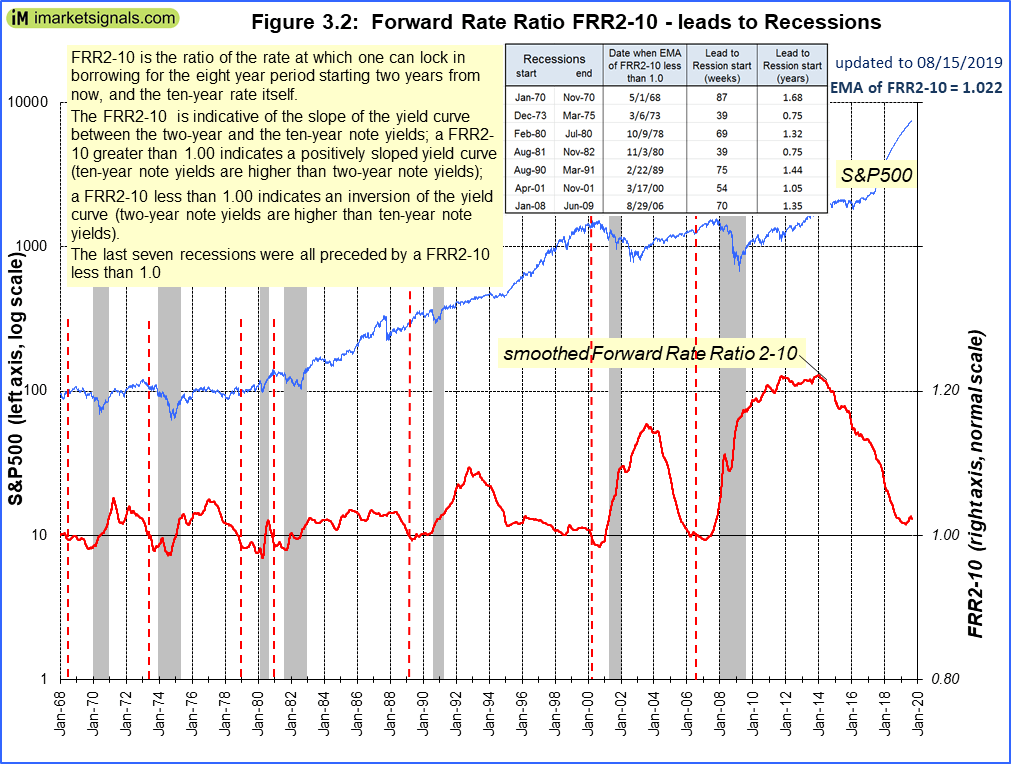

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is below last week’s level and is not signaling a recession.

The Forward Rate Ratio between the 2-year and 10-year U.S. Treasury yields (FRR2-10) is below last week’s level and is not signaling a recession.

A description of this indicator can be found here.

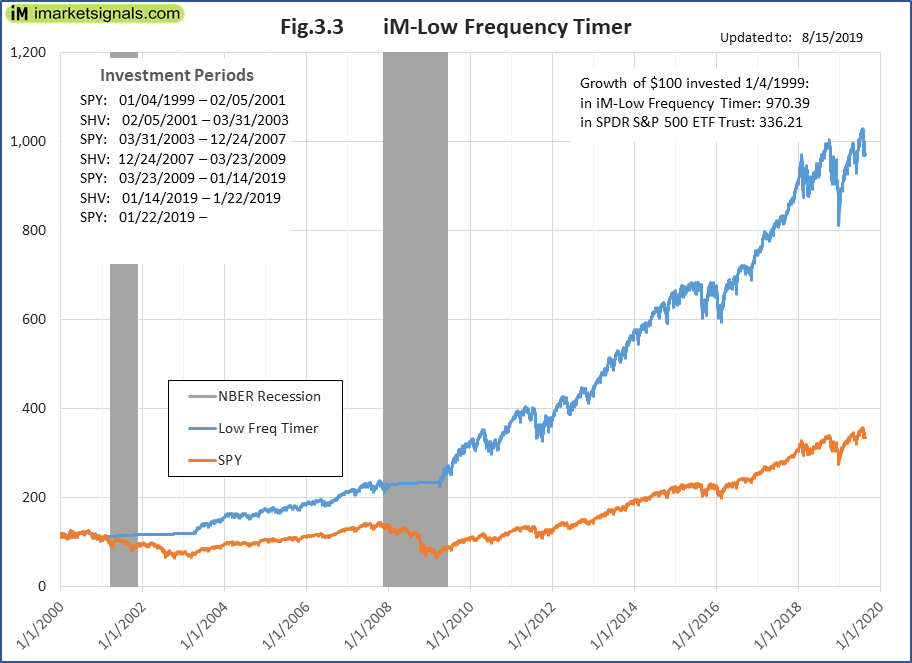

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

The iM-Low Frequency Timer is back in the markets since 1/22/2019.

A description of this indicator can be found here.

Leave a Reply

You must be logged in to post a comment.