The original Floor-Leverage Rule for Retirement, as proposed by Scott and Watson, calls for two parallel investments. The first one is to establish a low risk Spending Floor Portfolio with 85% of one’s funds. The second, the Surplus Portfolio, is an investment of the remaining 15% in equities with 3× leverage. If the Surplus Portfolio exceeds 15% of the total portfolio value at annual rebalancing when withdrawals are made, it is adjusted to 15% of the total portfolio value with the excess being transferred to the Spending Floor Portfolio. The problem is that 3× leveraged stock portfolios can lose most of their value. For example, they lost 94% from 2000 to 2008, which would have wiped out almost 15% of retirement capital if one had followed the Original Floor-Leverage Rule. A better approach, and one that could avoid such losses, is to time one’s exposure to equities as put forward by our Improved Floor-Leverage Rule, which is a low-risk spending and investment strategy for retirees.

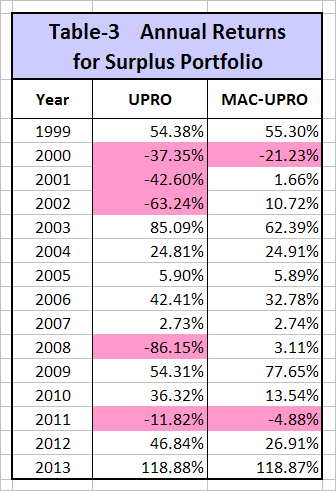

The analysis shows, that applying the MAC-System (backtested over 65 years) to time Surplus Portfolio investments in either 3× leveraged equities or Treasury bond funds would have provided fairly good returns. The annual returns for 1999 to 2013 are listed under MAC-UPRO in Table-3 in the Appendix and the performance is shown in Figure-1. The MAC-System is not some secret dataset to which only we have access. All the data is available to analysts and the buy and sell rules have been published several times, making the MAC easily reproducible.

The low risk Spending Floor Portfolio

For the analysis, the CREF Inflation-Linked Bond Account (CREFb) or the Vanguard Inflation-Protected Security Fund (VIPSX) appear to be reasonably low risk bond funds suitable for the 85% Spending Floor investment. The CREF Account was chosen because its inception was in 1997, whereas VIPSX was only available from the middle of 2000 onward. The investment period for this analysis is from Jan-2-1999 to Jun-30-2014. Over this period the CREF Account produced an annualized average return of 6.1% with a maximum drawdown of -14.3%.

The 3× leveraged Surplus Portfolio MAC-UPRO

The Original Rule calls for 15% of one’s retirement funds to be in a Surplus Portfolio holding 3× leveraged equities. The Improved Rule stipulates that the investment goes to the 3× leveraged UltraPro S&P500 ETF UPRO only for those periods when the MAC-System signals exposure to stocks; and during the other periods it goes to IEF, the iShares 7-10 Year Treasury Bond ETF.

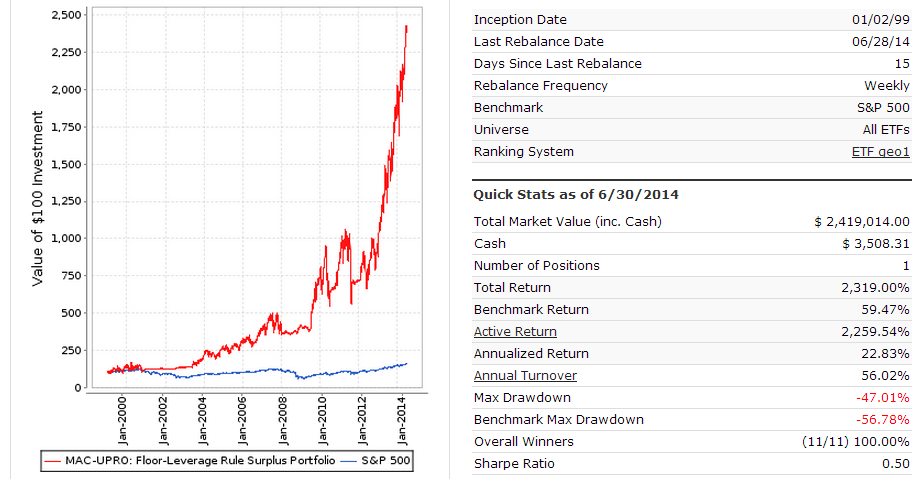

The Surplus Portfolio model, MAC-UPRO, without annual adjustments, was backtested on Portfolio123, a web-based portfolio simulation platform, from Jan-2-1999 to Jun-30-2014 and produced an annualized average return of 22.8% with a maximum drawdown of -47.0% over this period. There were only 10 realized trades and one unrealized trade, all of them winners. It is also tax efficient because on average a position was held for 477 days, and long-term capital gains tax would apply if not traded in a tax-deferred account. In Figure-1 the red graph shows the simulated performance of MAC-UPRO, and the blue graph represents the performance of the S&P 500.

Figure-1: MAC-UPRO Surplus Portfolio Model click to enlarge

click to enlarge

Returns from the Improved Floor-Leverage Rule Model

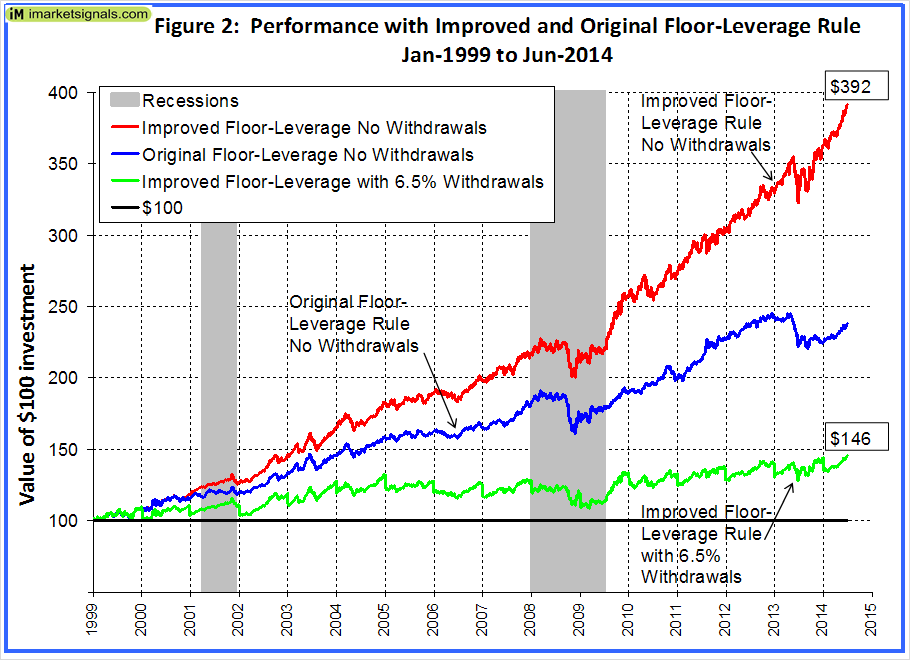

Assuming that no funds are withdrawn from the Spending Floor Portfolio, then the combined portfolio (85% Spending Floor and 15% Surplus) would have shown an annualized average return of 9.2% with a maximum drawdown of only -12.1%. The return is much higher than the 6.1% for the CREF Account alone, and the maximum drawdown is also better. The performance of an initial $100 investment following the Improved Rule is represented by the red graph in Figure-2, and can be compared with the blue graph, which depicts the performance when following the Original Rule.

Allowable Withdrawal Rate for Sustainable Real Spending

From Jan-1999 to Jun-2014, the annualized average U.S. inflation rate was 2.45%. Assuming that one would want to retain the real value of one’s retirement funds over this period, then for every $100 invested in January 1999 one would need to have $146 in one’s retirement account in June 2014.

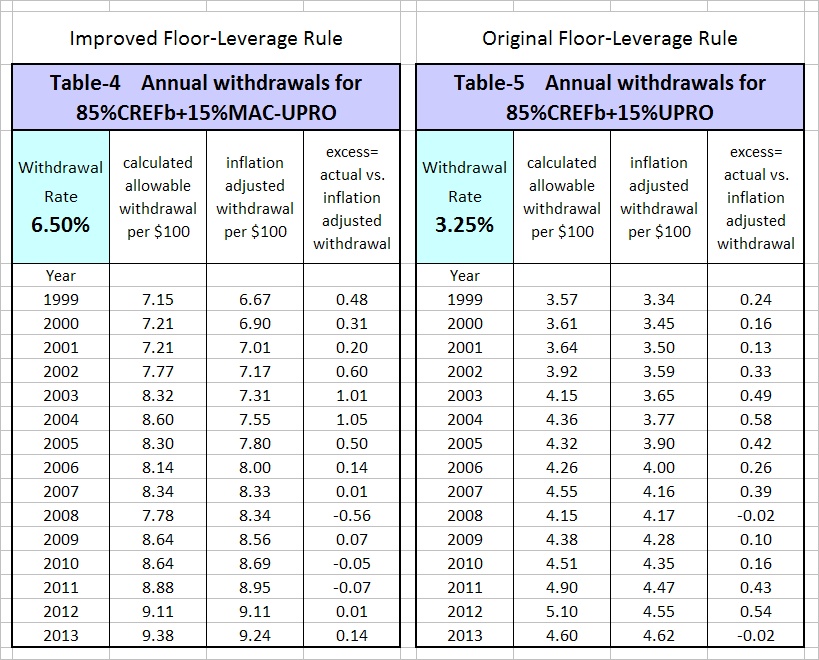

Following the Improved Floor-Leverage Rule (annually moving funds exceeding 15% of the total portfolio value from the MAC-UPRO Surplus Portfolio to the Spending Floor Portfolio; and simultaneously making one’s annual spending withdrawals), then the allowable withdrawal rate was found to be 6.5%. The performance over time is shown by the green graph in Figure-2 where the end of the year withdrawals are indicated by the vertical portions of the graph. Note that the remaining investment capital was always more than the $100 initial investment; and the end value was $146, the inflation adjusted value of the $100 starting capital.

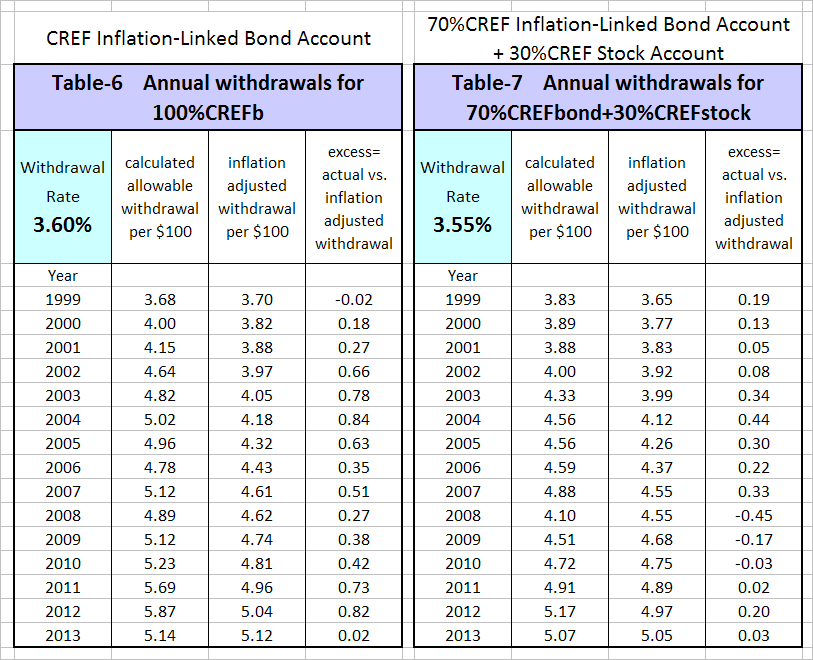

Similarly, if one had followed the Original Floor-Leverage Rule, then the allowable withdrawal rate would have only been 3.25% – exactly half of what the Improved Rule would have allowed. Had one simply invested in the CREF Account then one could have withdrawn 3.6% per year; and if one had invested in a life-cycle fund consisting of 70% bonds and 30% stocks then one could only have withdrawn 3.55%.

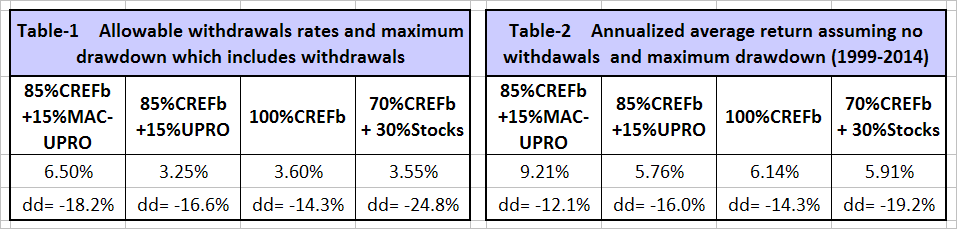

Table-1 lists allowable withdrawal rates and maximum drawdowns which includes annual withdrawals, and Table-2 lists annualized average returns and maximum drawdowns assuming no annual withdrawals were made, for the following four investment strategies:.

- Improved Floor-Leverage Rule (85%CREFb + 15%MAC-UPRO)

- Original Floor-Leverage Rule (85%CREFb + 15%UPRO)

- CREF Inflation-Linked Bond Account alone

- 70%CREF Inflation-Linked Bond Account + 30%CREF Stock Account

As one can see in Table-1, the Original Floor-Leverage Rule model produced the lowest allowable withdrawal rate. It would have been better to invest in the CREF Account alone. However, if one had followed the Improved Floor-Leverage Rule model one could have increased one’s annual withdrawals to 6.5%, which is significantly more than what the popular retirement strategy in use today, the 4% Rule, allows. Also, one would still at the end have had $146 left in one’s retirement account for every $100 of starting capital, i.e. a real $100.

It is also apparent that the popular life-cycle funds are not the low risk investments they are made out to be. A 70% bonds – 30% stocks fund would have produced the highest drawdown without a commensurate higher return. One can see from Table-2 that the Improved Floor-Leverage Rule strategy would have provided the highest return with the lowest drawdown; surprisingly a strategy which uses a high risk 3× leveraged ETF actually manages to be the lowest risk alternative of the four models.

Calculated annual withdrawal amounts for an initial investment of $100 are in the Appendix, Table-4, 5, 6 and 7. They are compared with inflation adjusted annual withdrawal amounts. For all four strategies sustainable real spending is preserved, because the annual calculated withdrawal amounts are in all cases on average higher than the annual inflation adjusted withdrawal amounts, while the real value of the initial retirement funds remained in tact.

Conclusion

Retiring in 1999 and using an investment strategy based on Scott and Watson’s Floor-Leverage Rule would have turned out to be a very poor decision. A retiree would have lost her entire investment in the Surplus Portfolio by 2008, 15% of her retirement capital. A 3× leveraged ETF would have lost 86% from January to December 2008 alone, when MAC-UPRO gained 3% over the same period. It is doubtful that a retiree “…was likely delighted that her loss represented only 13% of her total wealth…” to quote Scott and Watson. One can expect similar market declines in the future and, applying the Original Floor-Leverage Rule, this will almost guarantee a permanent loss of some capital during one’s retirement years.

Regardless of one’s retirement date, retirees with moderate to low risk tolerance should always be able to do better by following iM’s Improved Floor-Leverage Rule. This Rule uses the MAC-System (which seeks to identify up- and down-market periods) to time one’s investments in the 3× leveraged ETF. During up-market periods the 15% is invested in the 3× ETF would be equivalent to allocating approximately 45% to stocks. When the MAC-System signals down-markets the 3× ETF is sold and replaced with a 7-10 Year Treasury Bond ETF, providing a 100% investment in bonds for the portfolio during those down-market periods.

This strategy is easy to implement because there are relatively few transactions required. It should over time always provide better returns than holding the 3× leveraged ETF continuously in the Surplus Portfolio. Moreover, the simulated performance of an investment following the Improved Floor-Leverage Rule, from 1999 to 2014, a period with two recessions and two huge market declines (-49% to Oct-2002 and -57% to Mar-2009), shows that one’s initial retirement capital would not have been reduced by a 6.5% withdrawal rate.

Following the MAC-System

The MAC-System has been backtested over almost 65 years and has performed well over this long period. Weekly updates of the system are available on our website iMarketSignals.com every Friday.

Appendix

click to enlarge

click to enlarge

This is great work, Georg — kudos. Solid improvement on this concept. I wonder if there could be other variations on this as well for those slightly more aggressive. For example, take your 15% and allocate 5% to MAC-UPRO, 5% to UPRO-SH using your SPY-SH model, and 5% UPRO-TLT using your SSO-TLT model. Or overlay one of your portfolio management systems or your low volatility portfolios into the stock component.

–Tom C

Tom,

One can get better returns by using one of the ETF models instead of MAC-UPRO. For example Best(SSO-TLT) in the 15% Surplus Portfolio would provide a withdrawal rate of 7.7%. However, I approached this from the perspective of a retired person who wants a minimum amount of trading. Also the MAC-System has been backtested for 65 years with good results, and should continue to work well.

Also, “black swan” events do occur which no model can predict. I have tested the Floor-Leverage Rule with insurance on UPRO using put options. I will publish the results soon.

I am anxious to see what you have come up with by using put options as insurance. Do you know when you will be publishing that info? Do you have any plans on testing and publishing the results of using put options for protection with any of your other strategies or combo’s?

The Improved Floor-Leverage Rule with Put Option Insurance will be published this week (ending 8-8-2013). There are no plans to use put options with any other models.

Did you ever publish this? Can’t find it under 8/8 13 or 24. Thanks.